Comparison between Farcaster and friend tech: The Competition between Financial Socialization and Social Financialization

Author: defioasis

This article was written on May 13, and some data may have changed.

SocialFi, an emerging trend that combines social relationships and financial tokenization, evolves at the intersection of social networks and financial technology into two unique models: social financialization and financial socialization. Social financialization, with finance as the primary focus, wraps social networks in financial concepts and tokenization. It relies on the Ponzi model, allowing creators (content) to be tokenized and directly converted into economic benefits, represented by friend tech. Friend tech emerged in the second half of last year, leading a social trend with various friend tech applications springing up; however, after an initial surge, friend tech experienced a downturn, and various imitations have virtually disappeared. Recently, it regained attention with the release of v2 and the FRIEND token. Financial socialization, primarily through social platforms, builds communities and social relationships by producing content. Tokenization is embedded in everyday social activities through airdrops, rewards, and payments, creating potential economic value for every post, like, or comment made on the platform, represented by Farcaster. Strictly speaking, Farcaster is a social protocol layer rather than an application layer. The commonly referred to “Farcaster” is actually the Twitter-like social frontend Wrapcast built by the Farcaster team.

Applicable Scenarios

Farcaster and friend tech both belong to the social track, yet they fall into two major categories within it. Farcaster or Wrapcast operates like Twitter in the public domain of social networking, while friend tech is akin to WeChat in the private domain, with different usage scenarios potentially driving the evolution into two distinct models: financial socialization and social financialization. Public social networking emphasizes openness and visibility, user interaction based on content sharing, commenting, liking, and forwarding, as well as content discovery promoted through trending topics and recommendation algorithms. Private social networking emphasizes privacy and control, with interactions being more private and in-depth, usually occurring among known friends or members of private groups. This deep interaction helps maintain and strengthen existing social ties.

Corresponding to their characteristics and user behaviors, the implementation of tokenized incentives on public and private social platforms will have different strategies. On public social platforms, common incentives include rewarding users for creating and sharing popular content, rewarding participation such as likes, comments, and shares, and allocating tokens based on user activity and influence. Farcaster or Wrapcast, unlike some previous public social platforms, does not incentivize with potential token airdrops conducted by the platform itself but is instead initiated by the community and third-party applications. For example, active accounts on the Degen channel that have a specific number of followers and other criteria can receive Meme coins from the Degen community and other channel communities as rewards; Spectral conducts airdrops to active Farcaster accounts (defined as having more than 10 likes, 10 followers, 10 posts, and 10 to 200 contract interactions on Base). Users need to participate in interesting discussions and active atmospheres of the channels. Airdrops or incentives occur naturally rather than being targeted specifically at platform exploitation during certain periods.

It is worth mentioning that although Farcaster is a decentralized protocol, the Warpcast frontend has a moderation system that blocks nearly all pornographic or vulgar content, providing a good public environment for its users.

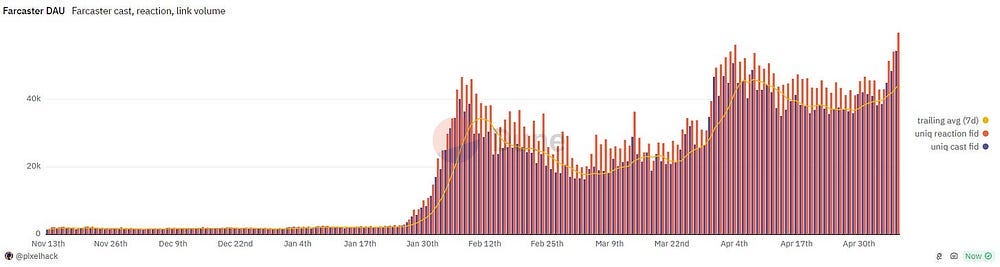

(Recently Farcaster DAUs also hit an all-time high

Data Source: https://dune.com/pixelhack/farcaster)

In private domain social platforms, a common incentive method is chat-to-earn, which has led to the creation of various low-quality contents. Friend tech, however, places the so-called “Earn” on where to chat, and the organic entry and exit are the core of friend tech. In friend tech, everyone can be a potential chat partner for others; when other users need to chat with someone, they need to purchase that person’s key. The value of the key is controlled by a bonding curve; simply put, the more people buy and the fewer people sell, the higher the value of the key. Half of the transaction tax generated goes into the protocol and the other half is distributed to the key holders. The newly introduced club feature in v2 is similar, essentially functioning like WeChat group chats, with entering and exiting the club being the core.

Little known is that Farcaster’s FID is essentially an NFT that can be resold, with FarMarket providing this support. After resale, the FID retains all the account data, including historical posts and followers. The highest transaction price for an FID to date has reached 3.69 ETH, over $10,000; some potentially high-value Farcaster accounts even ask for more than 300 ETH.

It is evident that the Farcaster protocol or the Wrapcast frontend application itself does not provide direct incentives. Whether users are incentivized or not is independent of the platform and comes from the community and third-party applications, constituting a light incentive model. Friend tech, on the other hand, incorporates strong incentives built into the application layer: the higher the floor price of the key, the more transactions, and the greater the incentives for creators, as well as the higher the platform’s revenue.

Entry Threshold

Friend tech became popular on CT relying on an invitation code system, with tens of thousands of users struggling to get a code in the early stages to access the platform. Using an invitation code entry model in the early stages of a new social network or service, especially by expanding the user base through seed users and key opinion leaders (KOLs), is a highly effective strategy. Initially, the official issues a certain amount of invitation codes to seed users and KOLs, who then generate more codes to invite their friends and followers, creating a chain reaction that gradually expands the user base. Each new user typically receives a limited number of invitation codes to further propel network expansion. Although the codes are free, leveraging hunger marketing and users’ FOMO (Fear of Missing Out) psychology can easily create buzz and topics within existing social platforms and communities. However, as the number of users increases, the congestion level to access the platform also eases.

Farcaster, on the other hand, adopts a pay-to-login system, with a basic annual fee of $5 for registering an FID ($3 via an invitation link), which is quite uncommon for a social platform. This has become a barrier deterring user entry after the initial enthusiasm waned, which is why even though Farcaster was launched last year, it has been lukewarm in popularity until this year, more a place for niche tech enthusiasts to interact. Strictly speaking, the $5 is not a fee to access the social network but a fee for renting storage space on the network, which is a core revenue for Farcaster. If the storage fee is not paid when due, the user’s social data will be cleared.

Overall, relying on an invitation code mechanism can attract user FOMO and stir up discussions on existing social platforms in the early stages of a social platform’s life, further enhancing the FOMO atmosphere. A pay-to-login mechanism, on the other hand, can act as a barrier to entry for uninformed users, with the additional educational and opportunity costs needing to be offset by other means. Of course, an appropriate threshold can exclude some studio and bot users.

Protocol/dApp Revenue

Farcaster’s revenue primarily comes from new user registrations, renewals by existing users, and payments for additional storage space, hence at this stage the growth of new users is directly linked to Farcaster’s income. Currently, Farcaster’s cumulative revenue exceeds $1.3 million, with daily fluctuations around $10,000; it has approximately 362,000 users.

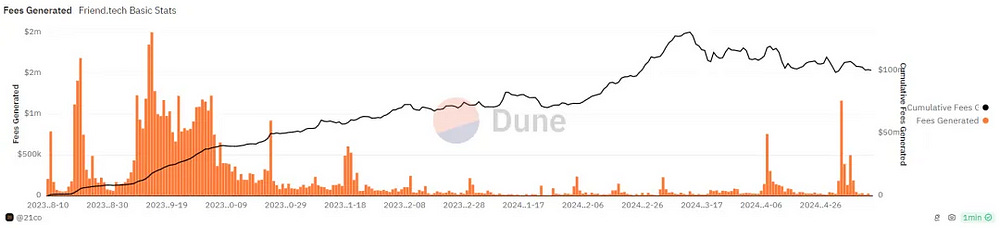

Friend tech’s revenue mainly comes from user key fees (charging a 10% fee per transaction). With the introduction of v2, additional sources include club fees, built-in swaps, and FRIEND LP fees, so its revenue is mainly related to the TVL and the activity level of transactions.

(Data Source: https://dune.com/21co/friendtech-analysis)

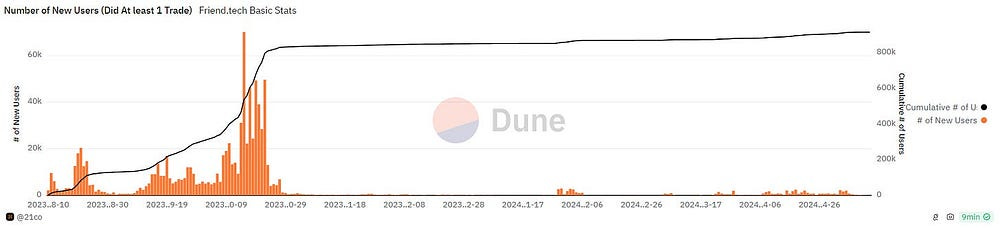

Friend tech has approximately 915,000 historical cumulative users, which is three times more than Farcaster. However, income derived from transaction fees is evidently more explosive than income from registration fees. Friend tech has captured over $100 million in historical cumulative fees, with half of that amount flowing into protocol revenue, meaning the development team has garnered over $50 million from the protocol. On September 14th of last year alone, friend tech captured $2 million in fees, meaning its revenue for just one day surpassed the cumulative revenue of Farcaster. High transaction taxes allowed friend tech to capture tens of millions of dollars in revenue within just over a month, leading to sudden wealth for the team. However, subsequent development and maintenance gradually stalled, leading to a prolonged period of downturn. It was not until the launch of v2 and the release of FRIEND that some attention was recaptured, but it is still far from its peak, and growth in new users remains stagnant.

The essence of friend tech lies in its bonding curve rather than the social aspect itself, and its development is constrained by the Ponzi scheme-like dynamics of the Ponzi model; Farcaster, by contrast, is more dependent on external VC funding for sustenance.

Asset Issuance And dApp Building

(Data Source: https://dune.com/whale_hunter/friend-tech-ultimate-analytics)

For friend tech, each of the 915,000 users represents an FT asset called a key, resulting in 915,000 key assets. Since the launch of v2 on May 3, over 200,000 clubs have been created (a user can create multiple clubs), corresponding to over 200,000 club key assets. In friend tech, all user profiles and group chat clubs are considered assets, with user keys primarily traded using ETH and club keys mainly traded using FRIEND. Currently, the overall market value of the 915,000 user keys is approximately $150,000 to $200,000; the total market value of the 200,000 club keys is around $10 million to $11 million, with two clubs valued over $1 million each. The native token FRIEND of friend tech was fully liquid upon launch, with a market cap of approximately $210 million.

Farcaster’s asset issuance is more diverse, mainly divided into three types. First, the user-registered FID is essentially an NFT, an asset that carries user social data, which can be traded on secondary markets like FarMarket. Second, social relationships generate social assets, mainly depending on channels; meme coins are a product of financial socialization, issued by channel communities. According to Farcaster Index data, there are 28 types of community Meme assets tracked, covering the Base and Zora chains, with a market value of approximately $880 million, of which DEGEN has a market value of $703 million. Third, assets are issued or applications built by Frame. Simply put, Frame is an embedded application that allows users to interact with third parties directly in Wrapcast without navigating to a third party website or signing transitions, which is easy and convenient to operate and at the same time passes on the user’s operational risk. Project owners can build directly on Frame, and users can use Frame to mint NFTs, play games, complete interactive tasks, and claim Meme coins. After Frame’s launch in late January and early February this year, Farcaster’s DAU and new user numbers grew more than tenfold. Additionally, Farcaster also has Wraps for tipping and payments (5u = 500 Wraps), which are not exchangeable in both directions; Syndicate, which received investment from a16z, has built the L3 Degen Chain using DEGEN as the native Gas token on Arbitrum Orbit.

Farcaster essentially serves as a Social Layer; the FID is a universal identity, and any developer can use the Farcaster protocol to build a frontend similar to Twitter or Reddit. Furthermore, like Mask’s social aggregator Firefly, it has already integrated posts from Farcaster and Lens. Currently, dozens of applications are being built around Farcaster to develop its social ecosystem, such as Launcher and Neynar, which are constructing Farcaster ecosystem components and were finalists in the a16z 2024 accelerator program.

Both Social Financialization and Financial Socialization have their advantages and disadvantages. Applications like friend tech, which represent Social Financialization, can attract massive participation through mechanisms similar to Ponzi model, due to their potential for rapidly increasing returns. However, excessive financial activities may lead to investment bubbles and unsustainable growth once user expansion slows, constrained by the nature of the Ponzi model itself. On the other hand, initiatives like Farcaster, which represent Financial Socialization, aim to make social interactions more engaging. They facilitate the flow of information along with value, building Meme community networks, and creating new seamless interactive experiences through Frame. However, the need for paid entry also poses challenges in terms of user education and acceptance.

Follow us

Twitter: https://twitter.com/WuBlockchain

Telegram: https://t.me/wublockchainenglish