FTX Case Update: How Are The Tokens Valued?

Author: Elven

A recent court filing revealed the details of FTX's crypto holdings. The presentation provides an overview of substantial payments made by the company, once the biggest global crypto exchange, to senior executives, including its founder, Sam Bankman-Fried, before its November bankruptcy filing. And an assessment of the value of the various asset classes currently held by FTX.

The value of cryptocurrencies held by FTX is critical to FTX's creditors, yet as seen in the documents, the value of some of FTX's cryptocurrency holdings is hard to put a value on.

Elven, a leading accounting platform for crypto assets, gives an interpretation from the court filing that might be helpful to investors and crypto firms to learn from:

How many crypto assets are held by FTX?

How does liquidity influence the valuation of crypto assets?

How are pre-ICO tokens valued?

How many crypto assets are held by FTX?

As of August 31, FTX held a total of $3.4 billion in crypto assets, consisting primarily of $1.16 billion in SOL, $560 million in BTC, $192 million in ETH, $137 million in APT, $120 million in USDT, $119 million in XRP, $49 million in BIT, $46 million in STG, $41 million in WBTC, and $37 million in WETH.

Besides that, FTX holds other illiquid tokens, crypto-related brokerage investments, and venture investments.

The chart shows that only 'Digital assets A' and 'Brokerage Investments' are listed with the exact valuation. The valuation of 'Digital Asset B' and 'Token Investment' is to be determined due to their illiquidity.

For 'Digital Asset A Holdings', their valuation is based on the price on August 31st. That introduces the critical method of evaluating crypto assets: Fair Value Measurement.

What is Fair Value Measurement

According to ASC (Accounting Standard Codification) 820-10-20. Fair Value is 'The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.'

Fair value measurement will replace the impairment method for crypto assets in this new proposed ASU (accounting standard update) from FASB (Financial Accounting Standards Board). Crypto assets will be listed separately on the balance sheet and measured at fair value, with changes in fair value included in net income. At the same time, holders of large amounts of a particular type of crypto asset must disclose their holdings in annual and interim financial reports.

For example, if you bought 1 Bitcoin at the price of $20,000 on Day 1 and it drops to $15,000 on Day 2, you must record a loss of $5,000. If the price is raised to $25,000 on Day 3, you still have to record a $5,000 loss under the impairment method. However, with fair value measurement, you will record a gain of $10,000 on Day 3.

Comment from Elven

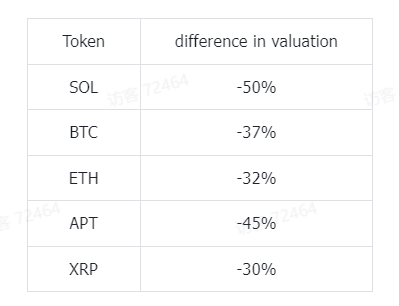

The valuation of crypto assets will be reflected more precisely under fair value measurement. If FTX uses the impairment method (which is not required for the filing), the valuation of crypto assets will be much less than the current result. The chart shows the difference of FTX's top holdings in valuation between the impairment method and the fair value method.

How does liquidity influence the valuation of crypto assets?

The second key point in the Overview is that crypto assets have been divided into 'Type A' and 'Type B' based on a specific liquidity threshold.

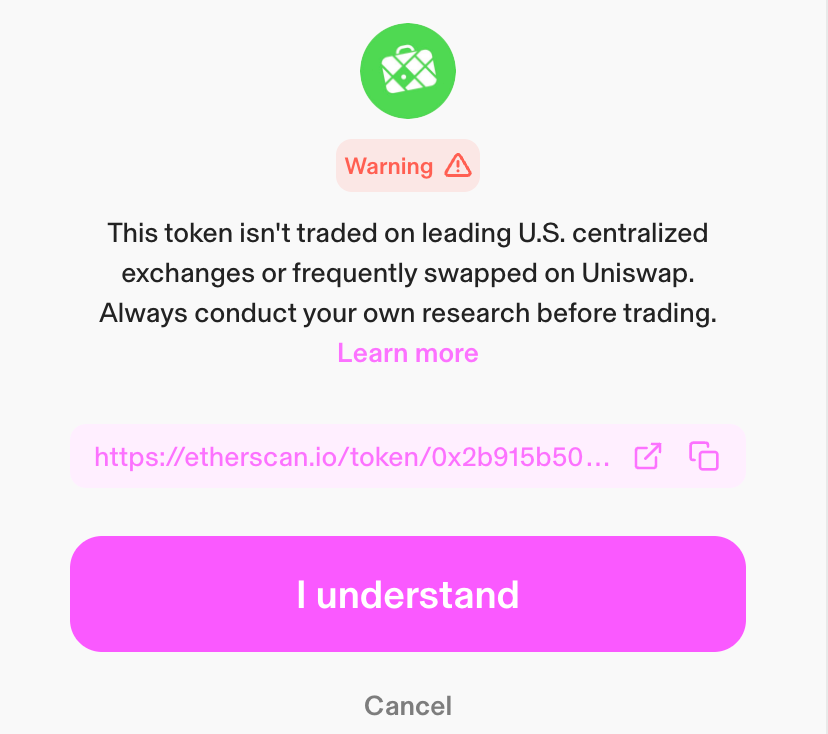

Let's use Uniswap as another example. When users want to trade the top 2 'Category B Tokens', warnings are sent to indicate lake of liquidity and risk of false valuation. And the standard is 'traded on leading U.S. centralized exchanges.'

Comment from Elven

Consideration of liquidity is important. Although the standard of liquidity is not expressed explicitly in the filing, we can look into the three-level fair value hierarchy in accordance with ASC 820-10-35-37:

Level 1: Observable inputs that reflect quoted prices (unadjusted) for identical assets or liabilities in active markets

Level 2: Inputs other than quoted prices included in Level 1 that are observable for the asset or liability either directly or indirectly

Level 3: Unobservable inputs

ASC 820 prioritizes observable data from active markets, placing measurements using only those inputs in the highest level of the fair value hierarchy (Level 1). So, the key variable is the existence of an active market.

According to ASC 820-10-20, the definition of active market is a market in which transactions for the asset or liability take place with sufficient frequency and volume to provide pricing information on an ongoing basis.

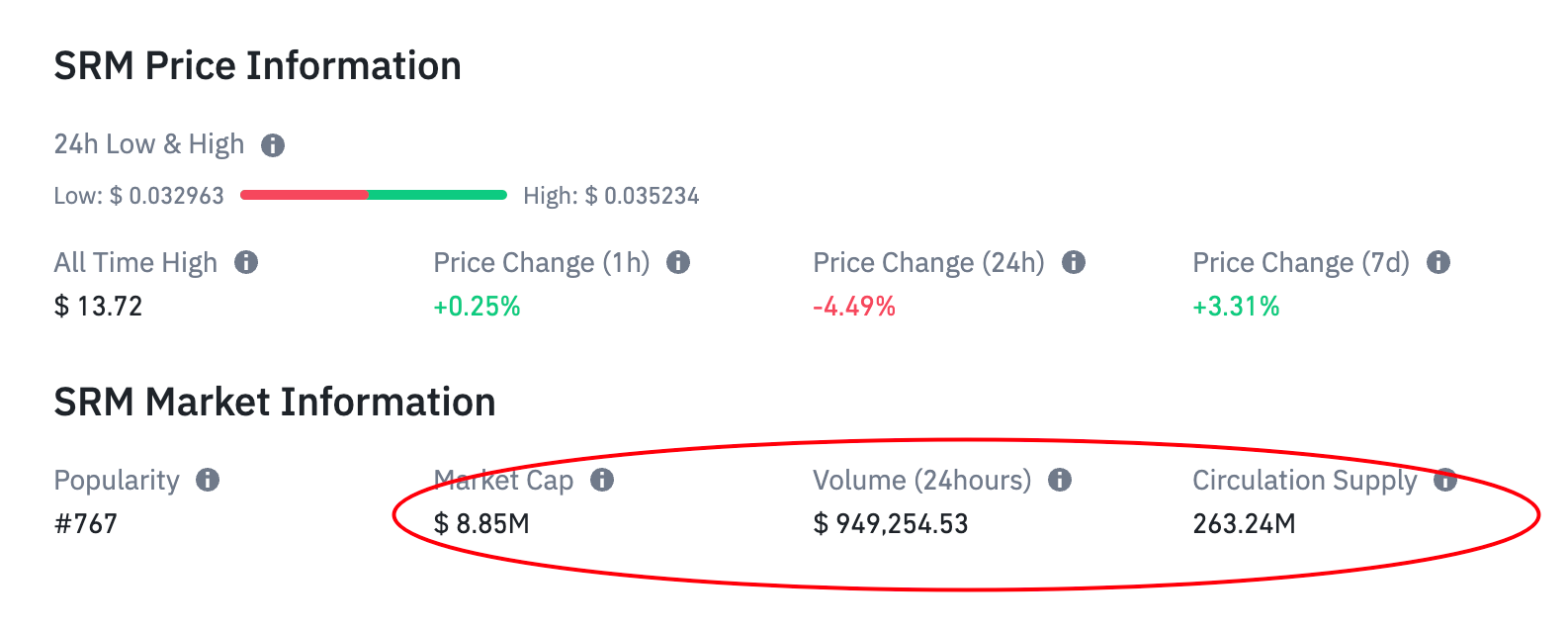

For scenarios like FTX case, we recommend looking at the market volume and the holdings of exact tokens. For example, as for SRM tokens, the trading volume takes around 10% of the market cap. It looks like the token is actively traded. However, the current circulation supply of SRM is much less than FTX's holding quantity (263M v.s. 9949M). That means the daily volume of the total market is around 0.2% of FTX's holdings! This problem is called 'Blockage'. It can be characterized as a specific type of liquidity discount relevant to large holders of a particular asset.

We could define the 'blockage rate' as the ratio of token holding to market circulation supply. A large blockage rate reflects that the market can not absorb the holding at the current value. Different discount levels could be put on different blockage rates, to ensure that the fiat assets obtained when the corresponding assets are actually disposed of are close to the estimate.

How are pre-ICO tokens valued?

The third key point is token investment. It mentioned that 'the cost basis of $506M should not serve as a proxy for recoverable value', introducing another important concept: cost-basis.

What is cost basis and why it matters

The cost basis refers to the initial purchase price when obtaining crypto assets. For instance, if you acquired one bitcoin on Day 1 for USD 20,000, your cost basis would be set at USD 20,000. The cost basis forms the foundation for computing profits and losses.

The computation follows a straightforward formula:

Cost Basis - Sale Price (Fair Market Value) = Gain/Loss

Although recording the cost basis for a specific coin is relatively uncomplicated, the complexity arises when you have to manage different lots (the one bitcoin you acquired is a 'Lot') in different platforms. Determining which cost basis to apply for calculating the gain or loss can become challenging when you decide to sell your crypto assets. It's possible that choosing one lot causes gain while another causes loss.

In FTX's case, token investments are divided into post-ICO and pre-ICO. Let's use the HOLE token as an example. FTX invested $68m for a given share of the token, so $68m is the cost-basis of FTX's HOLE token. However, the fair value (which is the 'recoverable value' in the filling) of the owned HOLE token might be much lower than $68m because of its illiquidity.

Comment from Elven

There is no available market data and related quoted prices for pre-ICO tokens. In this scenario, the income approach, which is based on future cash/token flows to the token holder, would be a possible method. It can prove particularly useful in token valuation, where prices are influenced by non-market activities such as SAFT.

There are three key elements in the income approach:

Future income estimation: Estimate the cash flows generated during the life of the crypto asset

Income generation period: How long could the token keep generating income

Discount rate: 1-conversion rate of the current value of future cash flows

For example, in this report given by Henley & Partners, the intrinsic value of Ethereum is evaluated by income approach. Transaction fees and new token issuance within a 20-year period estimate the future yearly income. When the discount rate is given by 13%, the intrinsic value would be $2,725. On the other hand, if we use a 19.19% discount rate, the implied price per ETH would be $1,349. Different assumptions will lead to a large difference in token valuation.

The same approach is used by RxR research in this article.

As we can see, different estimations of the three key elements would greatly influence the income approach, especially when the ecosystem behind the token is not as robust as Ethereum.

Brokerage and Wrapped Tokens

There are other valuable details in the report:

Bitcoin and Ethereum Trust Investment in Grayscale are valued separately from 'Digital Assets'.

Wrapped tokens are planned to 'be unwrapped and converted to the underlying native token to the extent possible'. Under the proposed ASU, wrapped tokens will not be under the scope of crypto assets. As a result, they can only be measured with fair value after unwrap.

Follow us

Twitter: https://twitter.com/WuBlockchain

Telegram: https://t.me/wublockchainenglish