Hyperliquid Guide: Disruptive Infrastructure or Overvalued Bubble?

Author | Joey @IOSG

Compiled by WuBlockchain

Over the past few months, Hyperliquid has attracted significant attention. This article aims to update everyone on the latest developments and expectations for the future. It is both an introductory guide to Hyperliquid and contains some nuanced insights into the overall ecosystem.

TL;DR

For readers who just want the highlights and key takeaways:

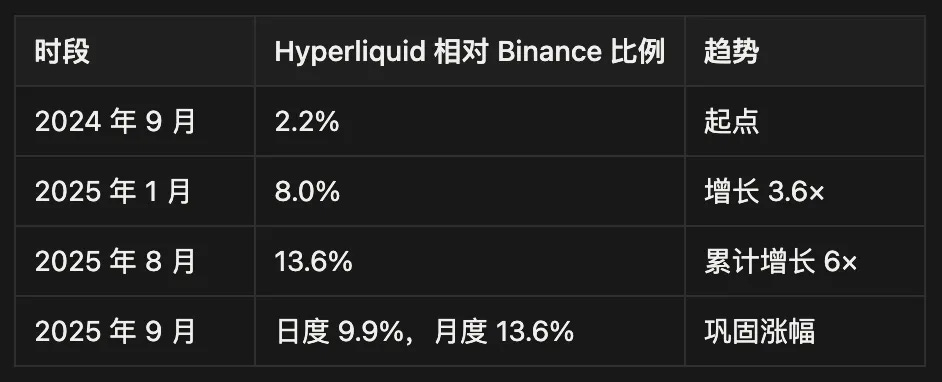

Hyperliquid has quietly taken 13.6% of Binance’s monthly perpetual futures volume, generating $116M in monthly revenue — but most analyses ignore the subtle risk/reward dynamics that will determine whether it becomes a breakthrough piece of infrastructure in crypto or just another DeFi casualty.

Market Position

● Accounts for 70% of decentralized perpetuals trading volume, with daily volume at 9.9% of Binance’s

● 665,000 traders generate $300K monthly trading volume per capita (65x Binance’s retail intensity)

● $4.4B in USDC locked on the platform, representing 71% of all USDC TVL on Arbitrum

Fundamentals

● $116M monthly revenue, with 97% redistributed to ecosystem participants

● 38% of total token supply (388M HYPE) still reserved for future growth incentives

● 24 validator nodes secure the network vs. Ethereum’s 1M+ (centralization vs. performance tradeoff)

Competitive Landscape

● Estimated 15–25% wash trading (better than industry average but still notable)

● Market share of Binance perps grew from 2.2% to 13.6% in 12 months

● Jupiter’s $32B in 60 days shows intensifying onchain competition in perps

While most people focus on token price appreciation, I analyzed its underlying business sustainability across multiple market cycles (including bear market stress tests and competitive pressure).

● Beginning at year-end, 238M tokens will unlock, creating $17M/day of sell pressure — 8x current buyback capacity. Most bulls ignore this structural headwind.

● A $600M Nasdaq-listed U.S. Treasury allocation and VanEck endorsement suggest non-retail demand might absorb unlock pressure, though institutional adoption timelines remain uncertain.

● Zero-gas trading, 0.2s block latency, and an inbuilt orderbook create switching costs — but technical debt and consensus limitations could erode these advantages.

Hyperliquid could face user attrition from token depreciation and yield compression, but its 97% revenue redistribution model and ability to generate sustainable income give it potential as a multi-cycle infrastructure project.

● Unlike traditional DeFi protocols reliant on token emissions or subsidized yields, Hyperliquid generates revenue from real economic activity and returns nearly all of it. This resilience shows when unsustainable yield models collapse.

● I expect a 60–80% drawdown during the 2025–2027 unlock phase, but business acumen and infrastructure advantages may enable it to emerge strong in industry consolidation.

This article goes straight to the real factors that will determine Hyperliquid’s long-term success: a sustainable business model, competitive positioning, and the ability to survive multiple cycles in an industry-wide extinction crisis.

What Happen?

As widely known, Hyperliquid is a leading decentralized perpetuals exchange (Perpetual DEX) now seeking vertical expansion. It captures 60% of decentralized perps trading volume, driven by regulatory arbitrage, airdrop incentives, strong UI/UX, deep liquidity, and robust community consensus.

Early Growth

Users could access a seamless UI/UX perps exchange without KYC (though still subject to local regulations). This was enabled by:

● Zero gas fees and low trading costs:Unique cancel/post-only order prioritization, superior to IOC and others, reducing toxic HFT sniping by 10x+. (See precompile details: x.com/emaverick90/status/1919727174426284488)

● Intuitive interface & one-click DeFi

● Ultra-fast trading: 0.2s blocktime, 20K TPS with a unique consensus model

● Strong MM & liquidity providers: bootstrapped initially by the core team

In a bull market where traders craved easy leverage (meme coins, prediction markets, derivatives, alt beta), perps found perfect PMF as the simplest gateway to leverage.

The Airdrop

Their airdrop reached ~94K wallets, with participants receiving $45K–$50K worth of HYPE on average:

● No insider sell pressure

● Wide distribution aligned loyalty & incentives

The Hypios community also granted extremely generous airdrops. Even Hyperliquid meme tokens ($BUDDY, $PURR) showed low sell pressure and sticky holders.

Traders/DeFi power-users staked tokens (for fee discounts) and deposited into HLP vaults, fueling a strong flywheel.

Heavy users, enriched by airdrops, kept trading actively — revenue funded buybacks — strengthening PMF and attracting more users and volume.

This massive distribution helped HYPE avoid the typical post-airdrop crash. In fact, HYPE surged +1179% from $3.90 (Nov 2024) to $47 (Aug 2025).

The HyperEVM

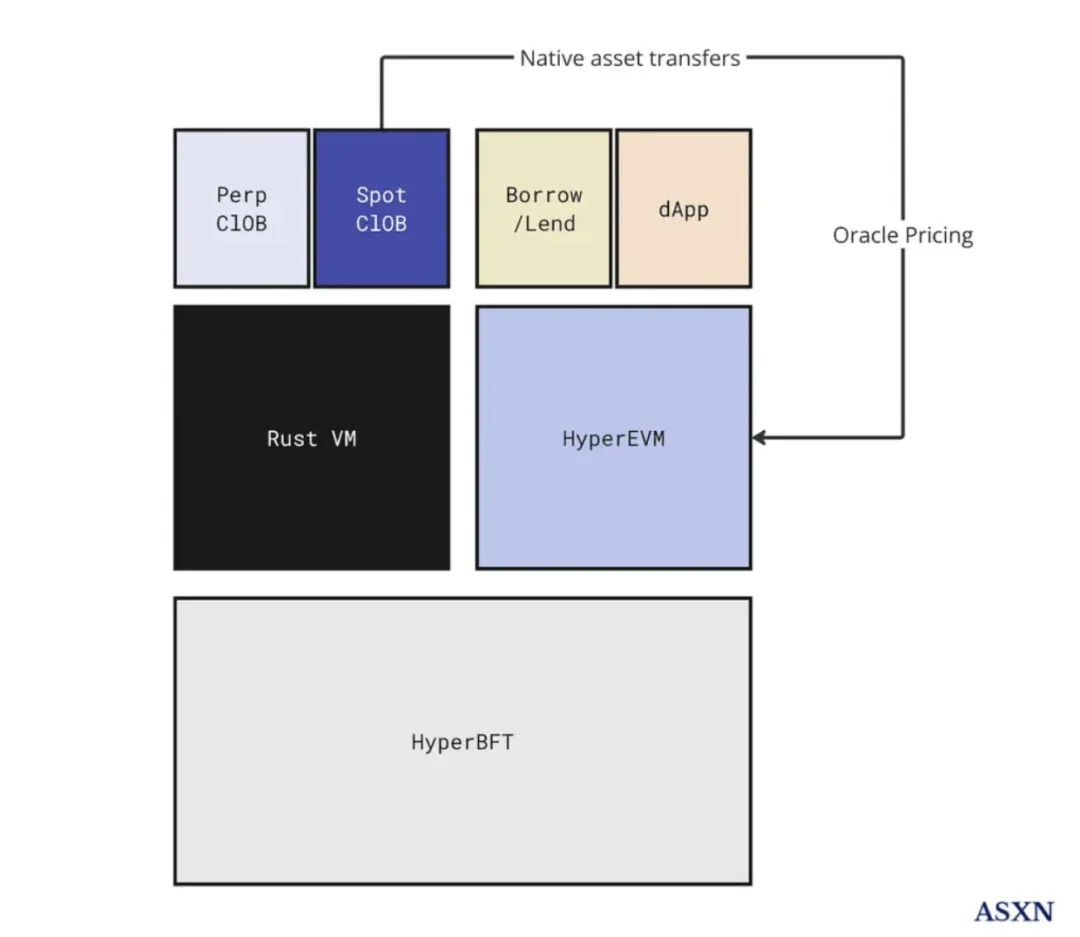

On Feb 18, HyperEVM launched.

It’s not a separate chain, but secured by HyperBFT (same as HyperCore). They share state and essentially run a blob-less Cancun fork.

Developers can now plug into a mature, liquid onchain orderbook. For example, deploy an ERC20 via standard EVM tooling, link it to HyperCore spot auctions, and trade the same asset across apps and the orderbook.

This expands use cases, empowers devs/community, and enhances liquidity programmability.

Notably, external projects are integrating: Pendle with HyperBeat, Kinetiq’s LST, LoopedHYPE’s WHLP & LHYPE, EtherFi launching preHYPE with HyperBeat, Morpho vaults curated by MEV Capital, Gauntlet, Re7 Labs, etc.

HyperEVM’s network effect is not about EVM cloning, but building a programmable financial OS where code, liquidity, and incentives are natively aligned and instantly accessible. Liquidity multiplies instead of fragmenting.

Hyperliquid positions itself as DeFi’s future “gravity center.”

What Now?

Having built liquidity and infra across farmers, quants, devs, traders, Hyperliquid asks: how to expand outward?

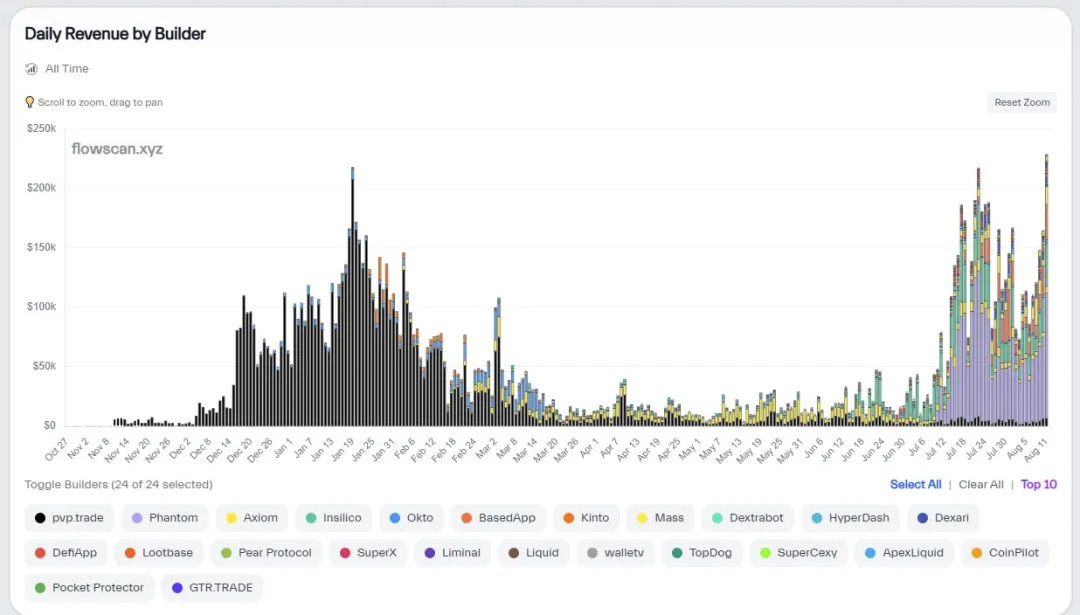

Builder Codes

let anyone integrate HL into distribution channels with revenue share (e.g., Phantom wallet’s 17M users).

HIPs (Improvement Proposals):

○ HIP-1: native token + spot orderbook standard

○ HIP-2: permanent liquidity injection for HIP-1 tokens (Unit project accelerating adoption)

○ HIP-3: dev-deployed perp markets (stake 1M HYPE, set parameters, fees, earn revenue share up to 50%).

By offering a more native spot trading experience, the Unit project has strongly driven the adoption of HIP-2. Essentially, Unit is a multi-signature wallet that allows traders to index the native chain and trade on Hyperliquid in a permissionless manner. (Learn more: https://docs.hyperunit.xyz/)

But arguably the update that drew the biggest response is HIP-3: https://hyperliquid.gitbook.io/hyperliquid-docs/hyperliquid-improvement-proposals-hips/hip-3-builder-deployed-perpetuals

HIP-3 introduces permissionless, developer-deployed perpetual markets at the core infrastructure level. Before HIP-3, only the core team could launch perpetual markets, but now anyone who stakes 1,000,000 HYPE can deploy their own market directly on-chain.

The process is as follows:

● Stake 1,000,000 HYPE

● Define market details: market name and ticker (still acquired via auction, similar to spot), choose collateral type, oracle source and fallback logic, leverage and margin parameters, contract specs and funding mechanism.

● Set the fee structure (set the base trading fee and any additional custom fees), decide the market deployer’s revenue share (up to 50%).Similar to the revenue-sharing relationship between Binance and Circle.

● Deploy the market: Market operators need to bootstrap liquidity themselves, while Hyperliquid receives the other 50% of fees (which flow back to the HYPE token). Note that these markets will not appear directly on Hyperliquid’s main interface, but anyone can choose which markets to connect to. This shifts Hyperliquid’s role from merely a launch platform to more of an asset provider.

Thus far, Hyperliquid has successfully tackled the following core areas:

● High-performance trading engine: delivers a trading experience for spot and perpetuals that effectively mimics centralized exchange performance.This includes leveraged trading and spot transfer functionality.A consumer-grade user experience combined with distribution channels.

● EVM as a programmable execution layer: a programmable layer (HyperEVM) built tightly around the UX and liquidity hub.

● Stablecoin infrastructure: successfully attracted USDH inflows worth $5.6 billion into its ecosystem.

For Hyperliquid itself or other projects within its ecosystem (built on HyperEVM), there remains vast room for future opportunities to explore:

● Native fiat on/off-ramps: building more convenient and low-cost bridges between fiat and crypto.

● Payment solutions: leveraging its high-speed, low-cost network to develop new payment applications.

● Web2-grade consumer applications: creating complex decentralized products with user experiences on par with traditional Web2 apps to attract a broader user base.

● Risk management engines: building better risk management and hedging tools for institutions and advanced traders.

Token/Liquidity Status

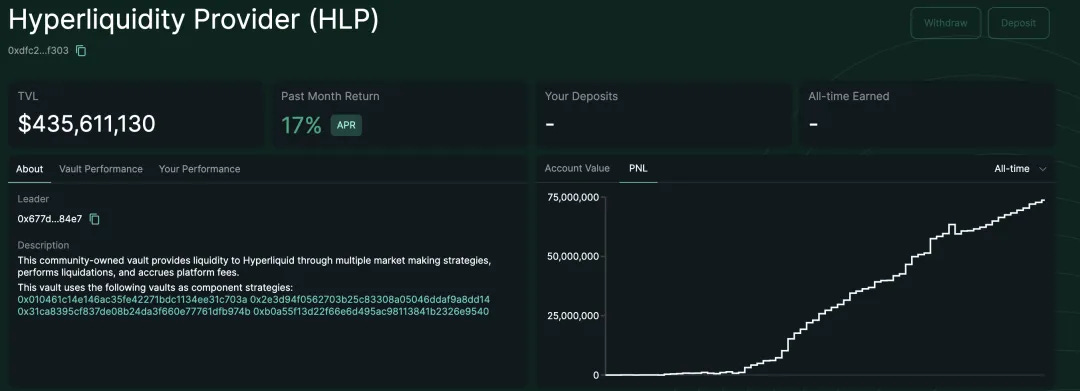

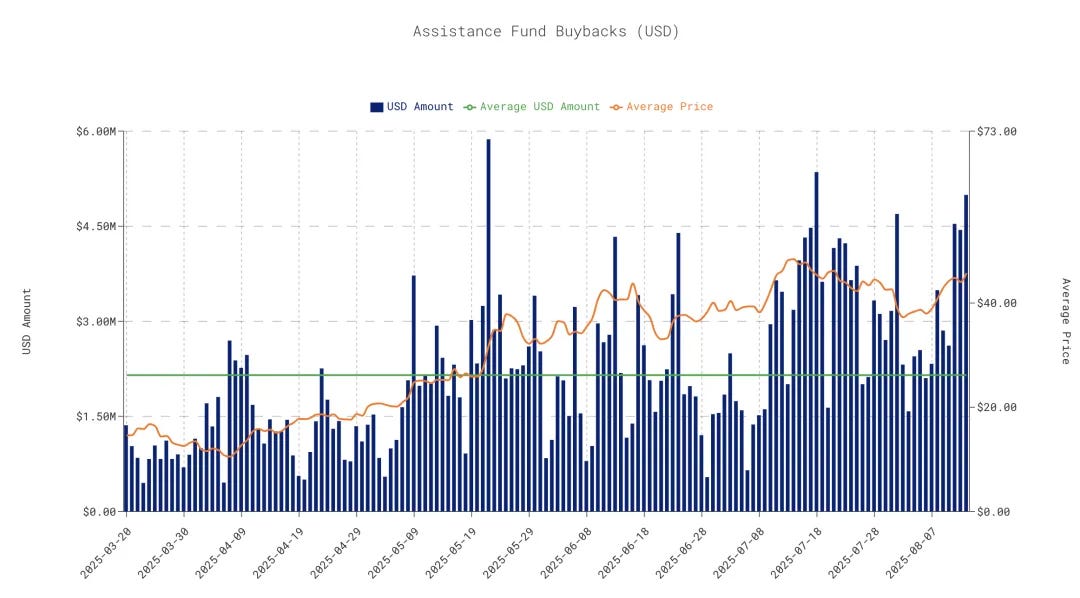

The buyback program led by the Assistance Fund shows that a total of 28M HYPE has been repurchased to date, funded by 54% of total revenue (46% of perpetual trading fees are allocated to HLP depositors, meaning that 92–97% of total revenue is returned to users). The average daily buyback amount reaches $2.15M.

Currently, 38% of HYPE’s total 1B supply remains dedicated to airdrops and incentives. While this has the potential to further drive ecosystem usage, it is a double-edged sword: such a large increase in circulating supply could create sell pressure far beyond current buyback capacity.

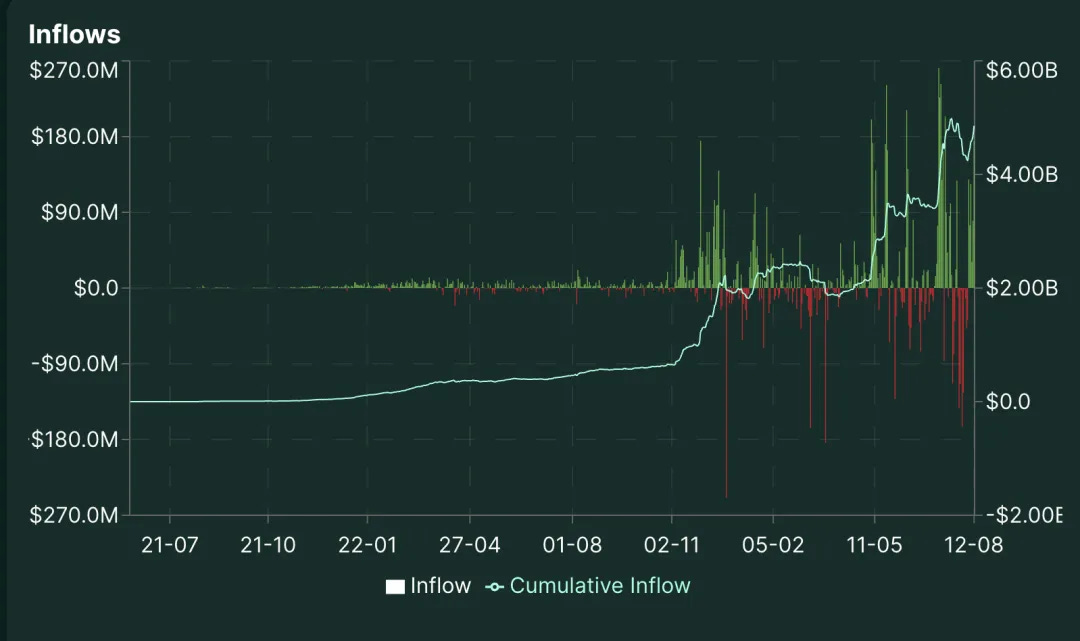

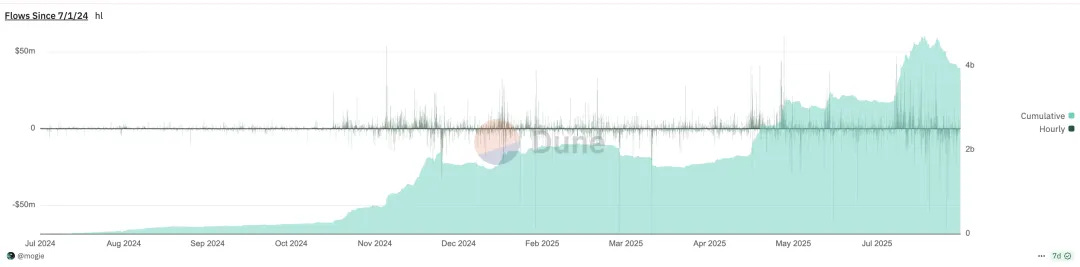

In terms of USDC inflows, Hyperliquid continues to grow, with a current balance of ~$4.4B. Remarkably, this accounts for 71.11% of all USDC TVL on Arbitrum, and these funds are being utilized within the Hyperliquid ecosystem.

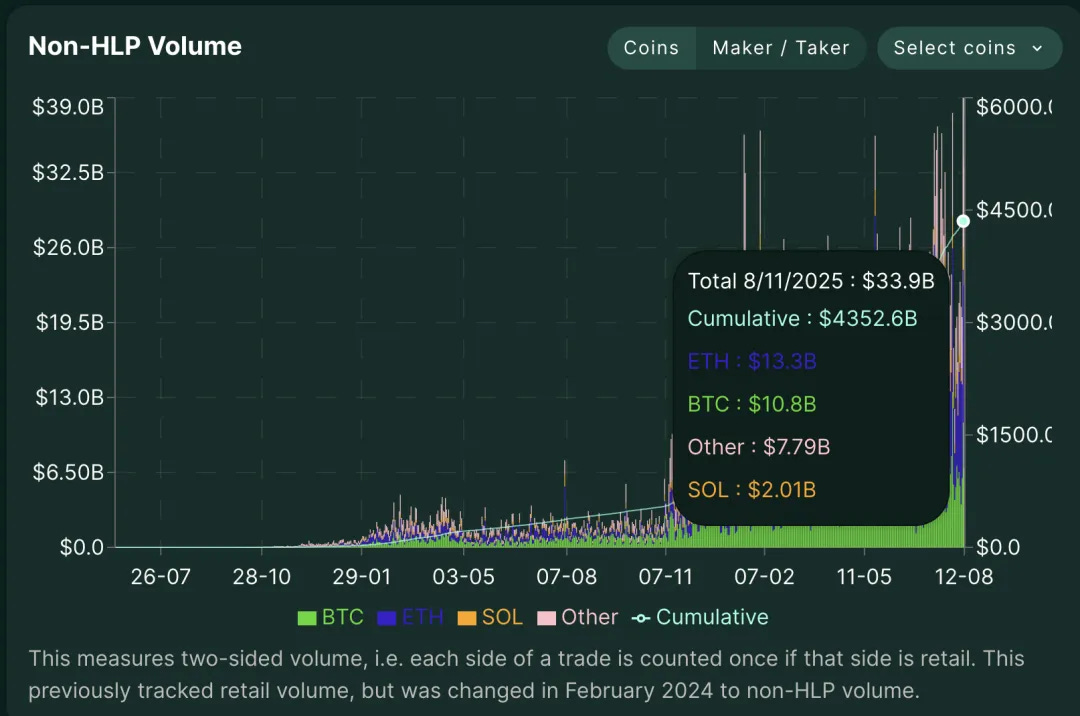

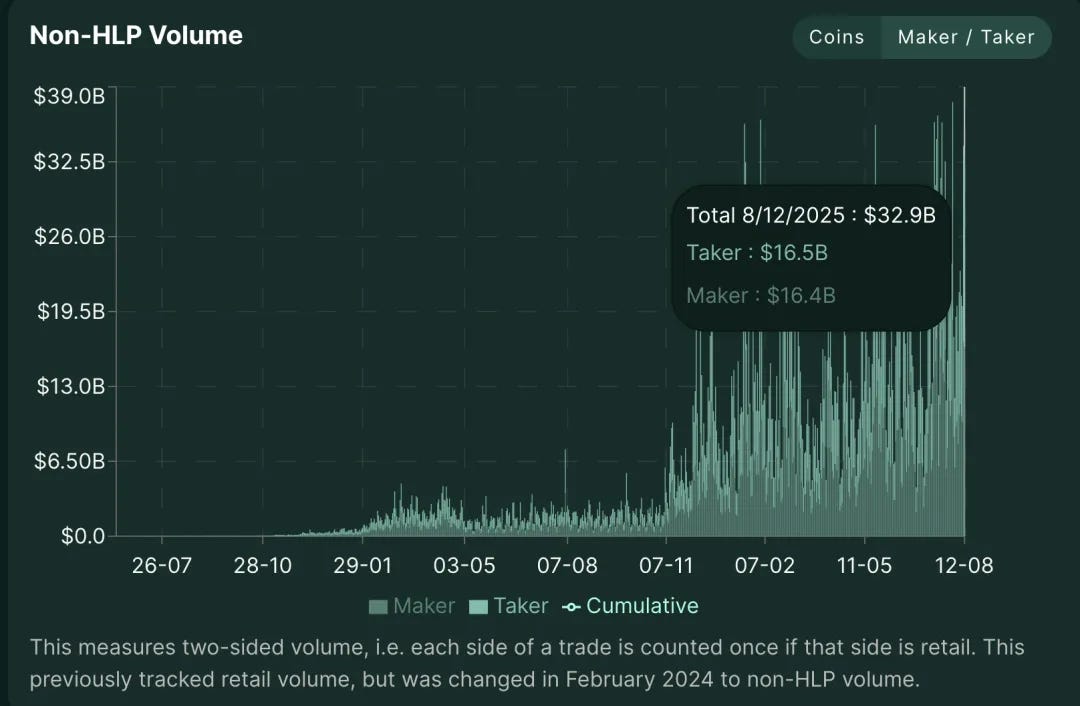

Using the non-HLP trading volume metric (cumulative $4.3T) for analysis: because HLP is a passive liquidity provider/platform pool, internalizing order flow and hedging risk, non-HLP volume represents peer-to-peer trading flow. It should be noted that this P2P flow still includes:

● Market makers

● About 20% of regular trade-mining accounts and vaults employing systematic strategies (see Appendix)

For an exchange, having more market makers is a “sweet problem.” In fact, Jeff once mentioned that there were already “too many” market makers.

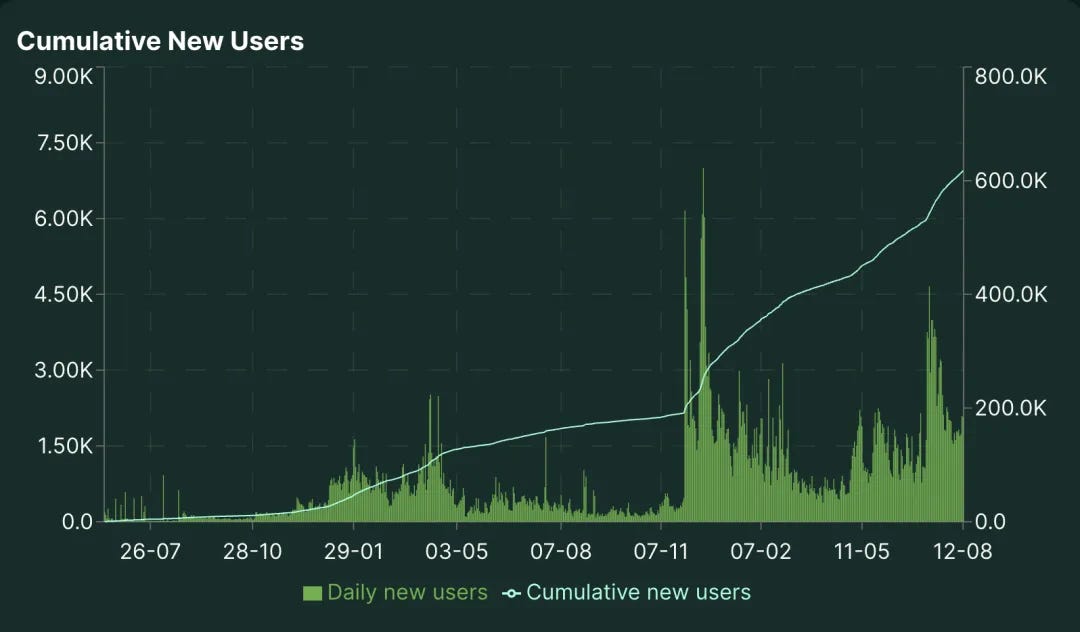

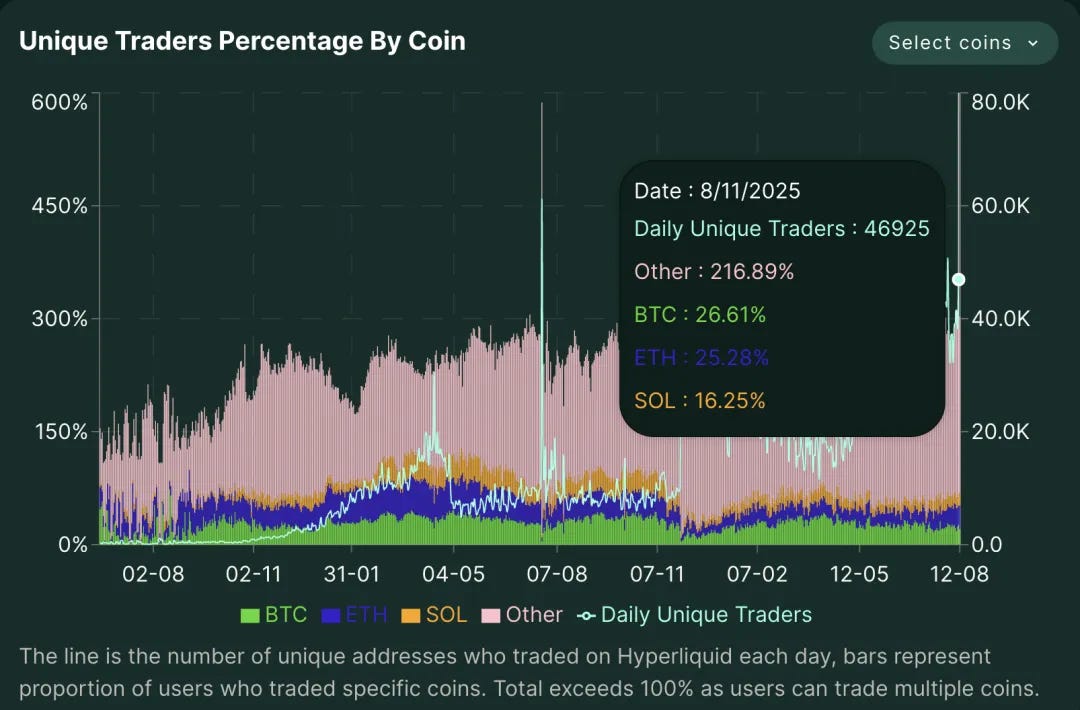

As of the date of analysis, daily active unique traders numbered 46,925. Statistics show that the total percentage of tokens traded exceeds 100%, since a single address trades multiple assets. This overlap of multi-asset trading implies Hyperliquid is not merely a single-asset venue—traders engage with multiple assets per session, indicating very high platform stickiness and cross-asset speculation. Meanwhile, the number of traders on Hyperliquid is steadily growing.

So, what does this mean?

At present, all components seem heavily reliant on funneling users into the HyperCore infrastructure and then returning value back to the ecosystem in some form:

● HyperEVM will bring more volume + a stable financialization layer to Hyperliquid.

● Builder Codes expand distribution channels, sending fees back to the HYPE token.

● HIP-3 enables permissionless market creation and shares fees with the HYPE token.

● HYPE token inflation benefits stakers and broadly delivers higher yields to HyperEVM.

With HYPE as both a perfect marketing tool and a community coordination mechanism, Hyperliquid has formed a tightly bonded, almost cult-like community. Ultimately, if leveraged trading remains a valuable experience for consumers, Hyperliquid’s flywheel will keep spinning.

What Next?

Bearish Case

Regulatory tightening risk

Perpetuals give end-users access to leverage markets. Without robust KYC/AML, there are money-laundering concerns. The platform may be forced to implement stricter compliance systems and report large trades. As with Polymarket, U.S. users may eventually need KYC to access the platform.

Token unlocks

Mishandling locked airdrop supply could trigger massive sell pressure.

● 238M core contributor tokens (23.8% of supply) begin linear unlock on Nov 29, 2025.

● At current prices, this equals ~$17.3M/day sell pressure in 2027–2028.

● Insider ownership would rise from 15.9% to a fully diluted 45.8%.Why it matters:

○ Current buyback capacity is only ~$2M/day

○ Unlock pressure is 8.6x buyback capacity

○ Unlocks coincide with a post-halving downcycle (2027–2028)

○ Maintaining price equilibrium would require 6–7x revenue growth

Liquidity fragmentation risk

With many new distribution forms (Builder Codes, HIP-3 markets), flow may divert elsewhere. Fees ultimately still flow back to HYPE, but revenue share may be diluted. HL controls core markets and channels, yet this risk remains.

Diminishing buyback effect & flywheel break risk

Buyback impact has diminishing returns. If adoption and revenue don’t match growth expectations or opportunity cost vs. other tokens, the flywheel may break (see April 2025 as an example). Game theory offers some mitigation—low market caps consolidate buybacks—but the key risk: how many users are on HL solely because of the HYPE token?

Security & trust gap

Retail loves HL’s UX, but Ethereum remains the preferred store of value: 800K+ validators vs. HL’s 16, longer security record, harsher slashing. HL’s design is secure but more centralized with concentrated risks. Events like $JELLYJELLY raised concerns about safety and governance.

Funding scarcity

With 97% of fees returned, there is zero budget for growth, marketing, or security incentives. Any attempt to redirect funds for development is a double negative for token holders. Competitors actively fund ecosystems; HL leaves itself “starved.”

Bullish Case

Growth momentum

● Capital inflows via EVM integration and interoperability

● HIP-3 markets attract institutional and retail flows from TradFi

● Perps market count continues expanding

● 38.8% of supply reserved for airdrops as growth ammo

USDH yield potential

~$5B USD deposits; USDH at current U.S. bond rates = $150–200M annual yield. If redirected from Circle to HYPE buybacks, it would be extremely bullish.

Cross-chain expansion

LayerZero integration: one-click deposits from any L0 chain (USDT0, USDe, PLUME, COOK). Breaks single-chain ceiling, capturing L2 orderflow first.

Fee advantage

● Current fee ~2.8bps vs. ~1bp competitors

● Zero-gas orders + onchain matching = sustainable profits

● Still profitable even if fees halved

CEX trust-crisis opportunity

After incidents like FTX, CEX reputations damaged. Hyperliquid, as semi-trusted neutral infra with CEX-like UX, narrows gaps on custody, costs, and regulatory arbitrage.

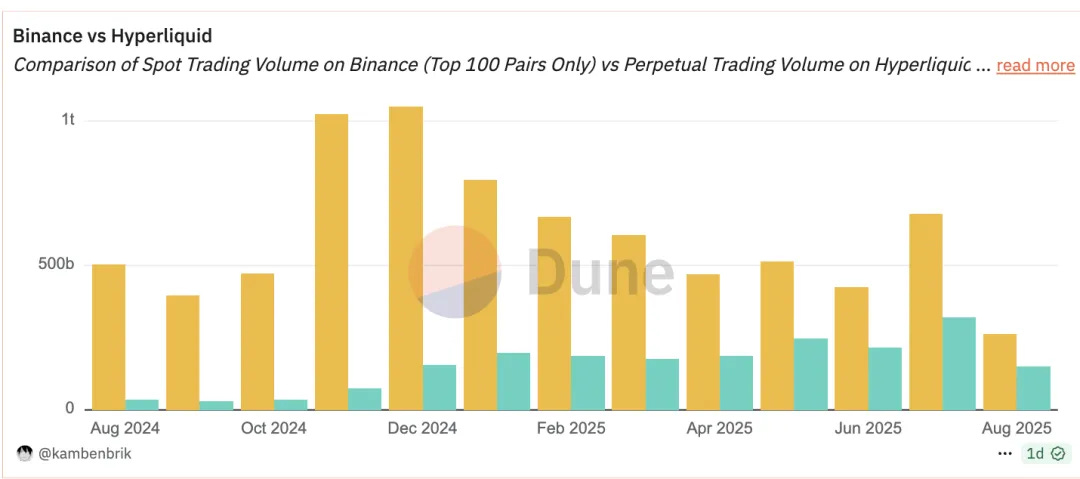

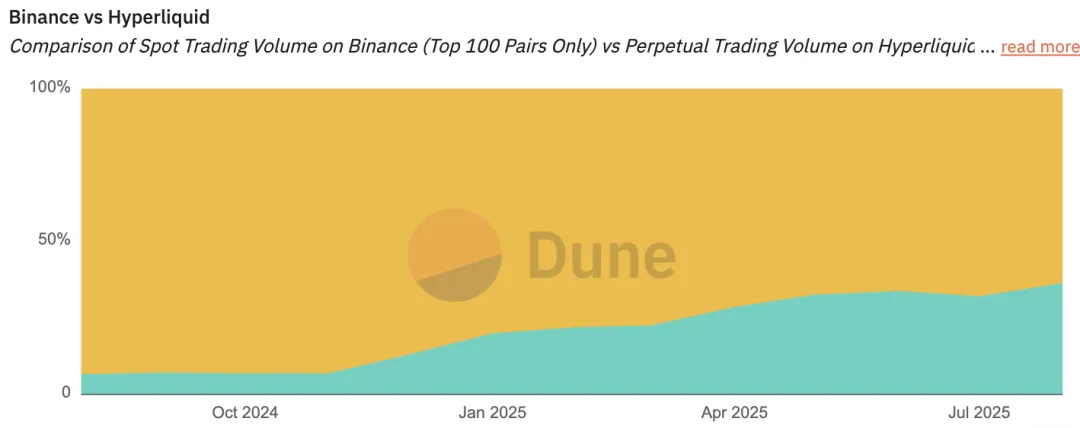

Still, comparing spot and perps directly is apples vs. oranges. Binance dominates off-chain retail; Hyperliquid dominates on-chain traders. Each rules its domain.

Daily Trading Volume (September 9, 2025)

30-day trading volume

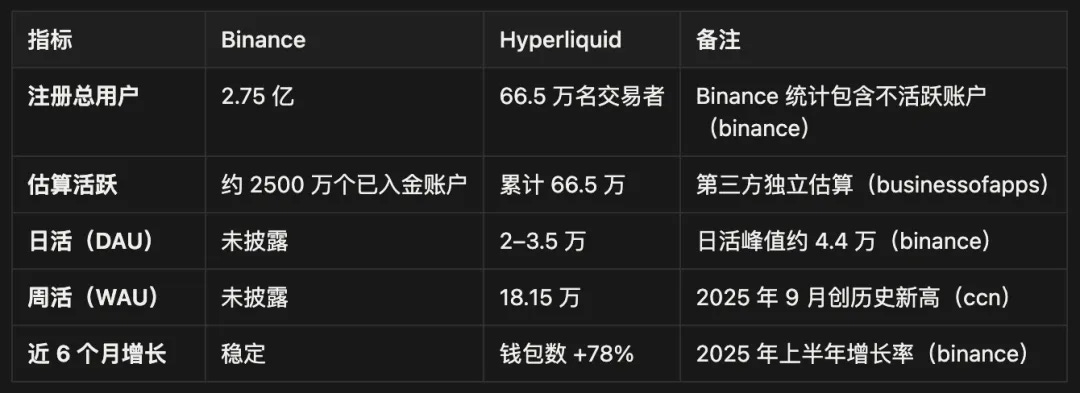

User base analysis

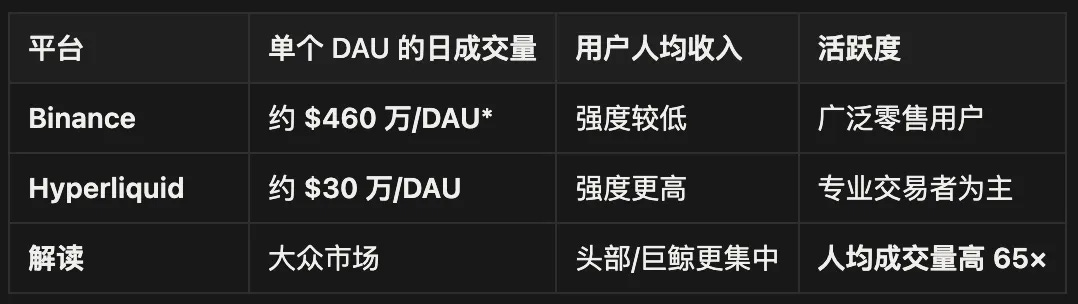

Trading intensity (based on ~25M active users rough estimate)

Market share

Every builder I’ve spoken with in the Hyperliquid ecosystem is heads-down, community-driven, and value-creating. This culture stems from how the ecosystem guided everything—from product to airdrops to community.

For crypto to go mainstream, new value and better experiences must be created for retail. Fundamentally, I believe Hyperliquid can deliver:

● Outstanding trading UI (an onchain Robinhood): seamless access to liquidity with a financial-grade experience.

● Pre-IPO products: perps-based pre-markets for speculation & price discovery, extendable to real Pre-IPO assets (see: ).

● Solving fragmentation: tools like https://superstack.xyz aggregate markets, just like 1inch did for DEX, Jumper for bridges, Beefy for yield farming.

● RWA: HIP-3 brings off-chain assets like SPX on-chain. Other RWAs offer sustainable, revenue-backed yields to grow the ecosystem.

In short, Hyperliquid takes a user-centric approach. From team decisions to thousands of aligned builders, the design ensures value creators—not extractors—win. Newcomers have equal opportunity to prove their insight in a rich, mature ecosystem, free of bad actors.

Whether a product can survive a bear cycle is anyone’s guess, but personally I’m optimistic about their ability to rebound and continue attracting builders.

This isn’t a bet on HYPE price or yield staying high—it’s a bet that real businesses with real users and real revenue ultimately win, even amid volatility and churn.

The market will likely give multiple chances to accumulate this theme at distressed prices. The real question: do you believe that in crypto’s long-term evolution, business acumen and sustainable revenue models matter more than short-term token games?

The upside is huge, and like any venture bet, I believe it’s in the right hands.