In summary: What is the real reason for the collapse of the FTX empire?

Written By: Colin Wu

Before the FTX empire collapsed, 99.9 per cent of us thought: maybe he had a lot of connected parties, maybe he was expanding too fast, but a collapse was "not so likely"?

After all, it has such a polished image as a leader in regulatory communication in the crypto world, the first choice of many institutional users, and the leading investor in a number of high-profile projects. In the days leading up to the crash, SBF paid out a generous $6m in compensation to several retail investors who lost money because of the API KEY leak, although third-party software, rather than FTX, may have been to blame.

When CZ and SBF announced Binance's acquisition of FTX to each other, the reaction was: Oh my God, something really happened to him.

When CZ then walked away, saying FTX's finances were too bad, it finally became clear that FTX was done.

What exactly caused the collapse of the FTX empire?

As more information comes to light, it turns out that the answer is as simple as c: borrowed too much money, collapsed during Luna, couldn't pay it back, and appropriated user funds.

(Alameda may not have lost money outright on Luna, but because Terra collapsed and lenders were chasing large amounts of loans.)

Alameda faced a barrage of demands from lenders after 3AC, a crypto hedge fund, collapsed in June, according to the Wall Street Journal.

In a video conference with Alameda employees late Wednesday Hong Kong time, Alameda chief Executive Caroline Ellison said, She, Mr Bankman-Fried and two other FTX executives, Nishad Singh and Gary Wang, were aware of the decision to send customer funds to Alameda. Singh is FTX's director of engineering and a former Facebook employee. Mr Wang, who previously worked at Google, is FTX's chief technology officer and co-founded the exchange with Mr Bankman-Fried.

FTX used client funds to help Alameda repay its debt, says Caroline Ellison. Lenders started calling in those loans around the time the cryptocurrency market crashed this spring. But the money Alameda spent was no longer readily available, so it paid with FTX client funds.

SBF explained to the New York Times that Alameda had accumulated a large "margin position" on FTX, which in effect meant it had borrowed money from the exchange. "It's a lot bigger than I thought it would be," he said. "In fact, the downside risks are very significant." He said the position was in the billions of dollars but declined to provide further details.

So the question is, why did they not shrink and close the loopholes, but continue to carry out large-scale investment and even rescue the so-called bankrupt enterprises? For this point, there is no detailed explanation from the media.

When SBF embarked on an acquisition spree this year, investing in struggling cryptocurrency companies, he did not share information with key employees, the New York Times reported. When he was told he was overextended and encouraged to hire more staff, he rejected the suggestions.

One possible judgment is that SBF wants to continue building the facade of expansion and complete the financing to get more money.

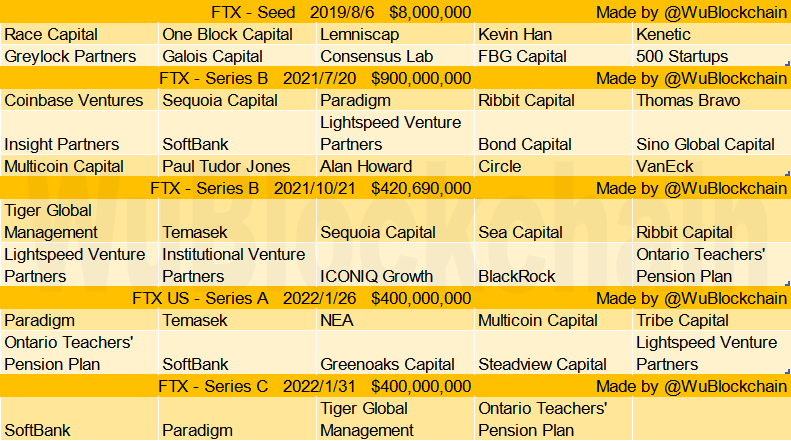

As you can see, FTX US also raised $400 million in early 2022 at a whopping $32 billion valuation. Oddly, FTX continued to tell the media that it was raising money. It was also difficult for the outside world to understand. After all, exchanges are a very profitable business on a regular basis, so why do you need to keep raising money?

Another possible explanation is that SBF is not so concerned about Alameda's multibillion-dollar breach that it may not be worried about a run on the exchange. For all intents and purposes, he did not think much of this risk until CZ began his attack.

It was only then that people realised how vulnerable the FTX was.

Internal management problems at FTX are also widely believed to have contributed to the collapse. As we often criticize: FTX emphasized that they only had 200-300 people and even in the days before the crash, were bragging that they had produced the highest per capita revenue/profit. But in terms of its ecology, which was once as big as Binance's, Binance has 7,000 employees. Obviously 200-300 people cannot properly manage such a huge company.

The opacity of FTX's decision-making and the SBF's clique culture were also seen as potentially problematic. Insider says, "I personally doubt that anyone other than Sam, Nishad, Gary and Caroline really knows the full picture of what's going on." When it comes to information cocoon, SBF can easily make wrong or even crazy decisions.

In conclusion, credit was used to carry out disorderly and wild expansion, internal management was out of order, and it could not be repaid when the market was down. The misappropriation of user funds was exposed as a "whistle". The FTX Empire crash, in fact, is that simple.

SBF had nearly $9 billion in liabilities and $900 million in liquid assets, $5.5 billion in "less liquid" assets and $3.2 billion in liquid assets, according to a filing with investors the day before the bankruptcy filing, according to Bloomberg. The "less liquid" assets include Serum, Solana and FTT. SBF had previously said it paid off $6 billion in assets, with a shortfall of several billion dollars.

Back in 2021, we ended our article describing SBF with this:

Dig deep: How FTX's SBF made billions of dollars in 3 years

"The magic of SBF lies in its extensive industrial layout and strong execution, which is beyond ordinary people. As a result, in only three years, SBF has accomplished what most people on the Forbes list have accomplished in decades. However, the SBF has also noted that most of his holdings are illiquid. I wonder if SBF can survive the bear market, or is it just a flash in the pan "legend" in this bull market cycle?"

Follow us

Twitter: https://twitter.com/WuBlockchain

Telegram: https://t.me/wublockchainenglish