Singapore's New Crypto Regulations Explained: Why So Harsh, Who's Affected, and Will It Trigger a Mass Exodus?

Author | @agintender、@Johnny_nkc、@alexzuo4

Compiler | Wu Blockchain

This document is for general informational purposes only and does not constitute legal advice, investment advice, or any other form of professional advice. Users should conduct their own independent review or consult a qualified attorney before taking any action based on this material.

Intro

On June 30, 2025, the Monetary Authority of Singapore (MAS) officially enforced the new regulatory framework for Digital Token Service Providers (DTSP), marking the formal rollout of a crypto asset regulatory regime that had been in development since its proposal in 2022. The implementation has sparked a wave of concern within the Web3 community, as the move is seen not only as a major shift for projects operating locally in Singapore, but also as a potentially transformative event for the entire crypto landscape across Asia. A large number of unlicensed entities may be forced out of Singapore, while a small group of licensed players—such as Coinbase, OKX, and HashKey—stand to gain significant advantages. Cities like Hong Kong, Dubai, Tokyo, Kuala Lumpur, and Bangkok are expected to become new hubs for those exiting Singapore.

Policy Background: A Three-Year Preparation Period That Went Largely Unnoticed

Singapore's regulatory overhaul of the crypto industry did not happen overnight, but was the result of years of planning. While the latest rules are widely perceived as a sudden and drastic regulatory crackdown. the Monetary Authority of Singapore (MAS) had in fact already brought Digital Payment Tokens (DPTs, i.e., cryptocurrencies) under regulatory oversight as early as 2020, through the Payment Services Act (PSA), which required entities offering crypto exchange and related services locally to obtain a license.

Subsequently, MAS identified ongoing regulatory arbitrage: some crypto firms were setting up operations in Singapore while serving only overseas clients—thus avoiding local licensing obligations. To close this loophole and align with Financial Action Task Force (FATF) standards, Singapore passed the Financial Services and Markets Act (FSMA) in April 2022. Part 9 of the FSMA specifically introduced a licensing regime for Digital Token Service Providers (DTSPs).

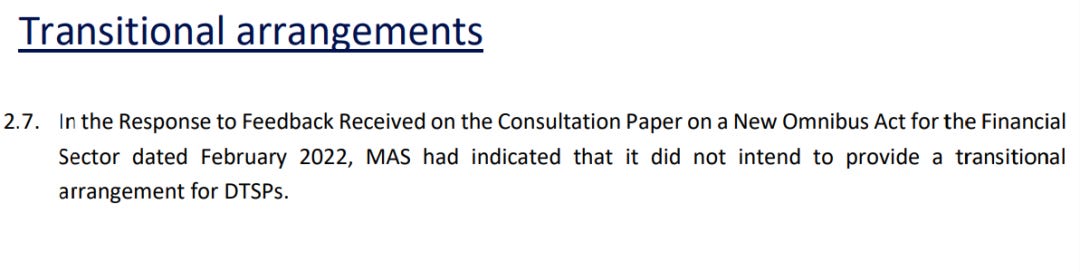

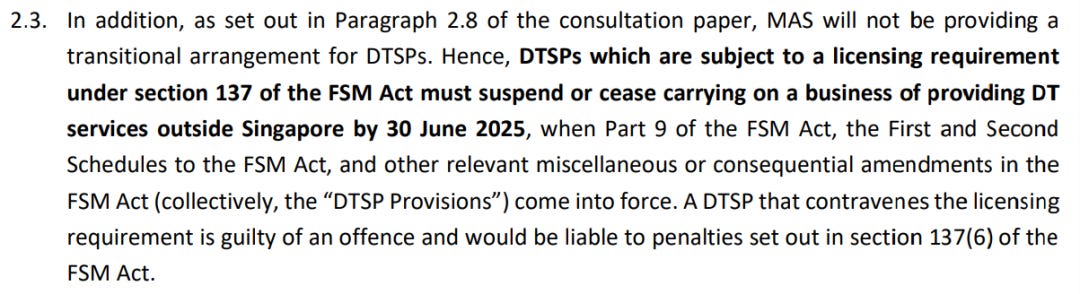

After passing the law, MAS did not immediately enforce it strictly but instead allowed a long lead time, with formal implementation scheduled for 2025. MAS had made clear in its published guidelines that there would be no transitional period.

In other words, from the passage of the law to its enforcement, Singapore provided the industry with nearly three years to adapt. Therefore, the MAS's recent announcement of the DTSP regulations was not a sudden and drastic regulatory crackdown, but rather the result of a long-established regulatory roadmap. However, the release of MAS's final response paper on May 30, 2025—which reiterated the firm June 30 enforcement deadline with no grace period—still sent ripples through the Asian crypto community. Some industry participants had hoped for regulatory leniency, but MAS's stance proved resolute, treating the past few years as a self-adjustment window for market participants.

Overall, Singapore's DTSP licensing regime was the product of a multi-year process involving extensive public consultation—such as the consultation report published in late 2024—and cannot be characterized as a sudden or unilateral policy shift. The formal legislation was introduced in 2022, refined through several rounds of feedback, and ultimately confirmed for enforcement in 2025.

However, due to limited attention from the Chinese-speaking community toward ongoing policy developments, many industry participants did not feel the regulatory pressure until the eve of implementation—resulting in panic-driven interpretations and public discourse around a so-called "Web3 exodus."

Key Provisions Explained

1.Definition of DTSP

DTSP stands for Digital Token Service Provider. According to Section 137 of the Financial Services and Markets Act (FSMA) and paragraph 3.10 of the relevant regulatory document, DTSPs fall into two categories:

Ⅰ. Individuals or entities conducting business from a "place of business" in Singapore;

Ⅱ. Singapore-incorporated entities that provide digital token services to overseas clients, regardless of where the actual operations are based.

2.Scope of Application: "In or From Singapore"

According to the above definition, both individuals and entities fall under the DTSP regulatory scope as long as they are engaged in digital token-related activities in Singapore, or if a company is incorporated in Singapore and provides crypto services to overseas clients.

Notably, the origin of the client base is no longer a determining factor: regardless of whether the service targets local or foreign users, any entity with operational ties to Singapore must obtain a DTSP license—otherwise, it will be considered operating illegally.

Examples include:

● The core development or operations team is based in Singapore;

● Servers or hosting infrastructure are located in Singapore;

● Marketing activities are explicitly directed at Singaporean clients;

● Receiving funds or assets from users in Singapore.

In short, offering services within the DTSP scope either in Singapore or to Singapore-based users requires a license.

3.The Broad Definition of "Place of Business"

MAS adopts a very broad definition of "place of business," which essentially includes any location where business activities are conducted. The authority has explicitly stated that a "place of business" may refer to any site used to carry out commercial activities, including temporary or mobile setups—such as a roadside stall.

As long as an individual is physically located in Singapore, whether in a corporate office, a shared workspace, or even on their own living room couch, engaging in digital token-related activities without a license is considered operating a business in Singapore—and therefore illegal. This clarification dispels the wishful thinking held by some: previously, many believed that working remotely from home for overseas crypto projects did not constitute a "place of business." MAS has clearly rejected this interpretation.

However, MAS does allow for some flexibility: if the individual is officially employed by an overseas company and is working remotely from Singapore, the regulatory obligation falls on the employer—the company must be licensed, while the individual is not required to apply separately.

The key issue lies in how the term "employee" is defined. For example:

● Does a startup founder qualify as an employee?

● What about equity-holding advisors?

These gray areas remain unresolved and may require further clarification from MAS through FAQs or future guidance documents. Nevertheless, the regulatory intent is unambiguous: to close the loophole of "being in Singapore while serving overseas clients." Even working from home does not exempt one from regulatory scrutiny.

4.The Scope of Covered Digital Token Services

In simple terms, anything related to "trading" is strictly regulated. Under the DTSP licensing regime, the scope of "digital token services" is extremely broad—encompassing nearly every aspect of the crypto business. According to the Schedule of the FSMA, there are ten regulated categories of activities, including but not limited to:

1) Issuance or Arranging Issuance of Digital Tokens

This refers to the creation or issuance of digital tokens on behalf of others, including activities such as IDOs, launchpads, and token generation events (TGEs).Any service involving the offering or sale of digital tokens falls under regulatory oversight.

This includes not only direct public token offerings by project teams (similar to ICOs), but also any behavior that induces or facilitates others to buy or sell tokens.

In short, both issuers and intermediaries engaged in fundraising or token promotion must be licensed.

2) Custody Services for Digital Tokens

This refers to holding or controlling clients' digital tokens, including both cold and hot wallet solutions.Whether providing secure vaults, custodial wallets, or executing token-related instructions on behalf of clients (such as operating their accounts or executing trades),any service provider with control over tokens or their access mechanisms is subject to regulation.

This also includes offering secure interfaces or systems that allow clients to access and manage their assets.

3) Brokerage, Matching, and Exchange Arrangement Services

Operating centralized or decentralized order books and trade-matching services (including OTC and DEX aggregators)These cover platforms facilitating the purchase, sale, or exchange of digital tokens, as well as brokerage services that match counterparties,

such as offering UI/UX trading interfaces to help buyers and sellers complete transactions.

4) Transfer or Payment Services

This includes any service that facilitates the transfer of digital tokens from one wallet or account to another on behalf of clients—meaning that intermediaries involved in such transfers, including cross-chain bridges, must also be licensed.

Examples include payment gateways, bridging protocols, and wallet providers offering "transfer on behalf of users" functions.

5) Validation / Governance Participation Services

This refers to participating in node validation activities on behalf of clients—such as staking in a customer's name, running validator nodes, or voting in on-chain governance processes.

It also includes receiving rewards or compensation derived from staking or governance participation.

6) Technology Enabling Custody Services

This covers infrastructure or technical services that enable custody, such as MPC (Multi-Party Computation) wallet providers, key escrow services, and API developers supporting custodial platforms.

Even if the provider does not directly control client assets, their role in the control process is considered material, and therefore subject to regulation.

Taken together, these provisions demonstrate that the DTSP licensing regime covers virtually all services throughout the digital token lifecycle—from issuance and trading, to transfers, custody, and operational participation. No activity is exempt from oversight.

Which Activities Do Not Require a License?

1.Pure Advisory / Consultancy Services

This includes activities such as project design, tokenomics consulting, legal structuring advice, and product development guidance.

As long as you do not engage in asset custody, token issuance, or trade execution, such advisory roles do not fall within the scope of DTSP regulation.

2.Marketing / Publicity Services

This refers to community management, advertising, brand design, and other promotional services.

Even if you help a Web3 project with market outreach in Singapore, as long as you are not involved in token distribution, trade facilitation, or asset control, you are generally not subject to DTSP licensing. However, if you directly coordinate token sales, distributions, or transfers on behalf of a client, regulatory obligations may be triggered.

Assessing the Regulatory Shift: Why MAS Moved from Leniency to Stringency

Web3 is not a lawless zone. Any business involving trading or financial flows is subject to regulation—regardless of jurisdiction. What sets Singapore apart is the forward-looking nature of its policy framework. The strictness of the new DTSP regime lies not only in its uncompromising enforcement but also in its high bar for market entry. Behind this are both external triggers and MAS's long-standing regulatory philosophy:

1.Singapore's Regulatory Culture: "Everything Requires a License"

Singapore enforces a finely tuned licensing regime for virtually all commercial activities:

● Street hawkers must undergo regular training and obtain a hawker license;

● Even a café playing background music must apply for a public broadcast permit;

● Opening a hotel does not grant automatic permission to operate a swimming pool—an additional license is required.

Singapore's so-called "crypto-friendly" environment does not mean absence of regulation.In fact, the crypto industry is treated the same as others: "certification before operation, periodic reviews, and strict licensing compliance." At its core, Singapore's regulatory model is registration-based, not laissez-faire.

No matter what business you're in, regulatory oversight is always a given.

2.Investor and Capital Protection as a National Mandate

Singapore's government operates in a paternalistic model, placing high emphasis on citizen welfare—especially in the realm of financial security. For instance, the government restricts access to retirement funds under the CPF (Central Provident Fund) scheme until the age of 55 to ensure long-term financial well-being.

MAS, for its part, prioritizes investor protection within the crypto licensing framework.

It places strong emphasis on AML/KYC compliance, minimum capital requirements, and insurance provisions, ensuring that if something goes wrong, there is clear accountability and financial recourse.

Operators must be identifiable and backed by sufficient collateral or insurance coverage.

3.The "Fujian Gang" S$3 Billion Money Laundering Case: A Regulatory Red Line

A key driver behind MAS's latest regulatory tightening is the need to prevent cross-border financial crime and money laundering. Digital token services are inherently cross-border in nature, often conducted over the internet with high anonymity and rapid fund mobility—making them attractive tools for illicit actors engaged in money laundering or terrorism financing.

Singapore has faced this risk firsthand. The most high-profile case in recent memory was the 2023 "Fujian Gang" cross-border money laundering scandal, which involved ten foreign nationals from China's Fujian province and other regions.

The individuals laundered funds on a massive scale by setting up companies and bank accounts in Singapore. The total amount involved exceeded S$3 billion, making it the largest money laundering case in Singapore's history.

Due to the severity of the case, it even had ripple effects on public sentiment during Singapore's general elections.

Contrary to popular belief, MAS is not primarily concerned with reputational damage from fraudulent platforms. The Singapore government is highly experienced in managing such incidents. What truly concerns regulators is the flow of illicit capital that could trigger diplomatic fallout or threaten Singapore's role as a financial safe haven in Asia.

This focus is evident in the MAS Investor Alert List (IAL) (https://mas.gov.sg/investor-alert-list)—a tool to identify suspicious entities but also a signal of deeper regulatory concerns about cross-border capital movement.

4.The "Strict Entry, Strict Oversight" Licensing Regime: Deconstructing the Illusion Through Practice

MAS's hardline stance is also reflected in its stringent licensing thresholds. According to its published guidelines, MAS stated that it would consider issuing a DTSP license "only in exceptional circumstances", and outlined a set of near-onerous approval criteria:

● Applicants must demonstrate a commercially viable business model, with a compelling justification for operating in Singapore without serving the local market. In other words, MAS must be convinced why the applicant intends to serve only overseas clients from Singapore.

● Applicants must reassure MAS that their operating model will not raise regulatory concerns, and must already be licensed or supervised in all foreign jurisdictions where they offer services, complying with international regulatory standards—such as those of the Financial Stability Board (FSB), IOSCO, and FATF.This means the applicant must be compliant in every country where it has customers—a virtually impossible requirement for many early-stage Web3 projects.

● MAS also emphasizes that the applicant's organizational structure and compliance capabilities must not raise red flags, requiring strong corporate governance and sufficient personnel and financial resources to fulfill regulatory obligations.

As a result, when MAS opened applications in 2021, over 500 entities rushed to apply at the peak. However, less than 10% were approved, due to weak qualifications.

By the end of 2024, only 13 firms had been granted a Major Payment Institution license for Digital Payment Token (DPT) services, with the total number of licensees increasing from 16 to 29.

Compounded by MAS's limited supervisory bandwidth, the approval process has become even more selective.

5.Web3 Has Yet to Deliver "Sticky" Economic Benefits to Singapore

Despite the large-scale influx of Web3 projects into Singapore, the sector has failed to generate long-term, localized economic value. Many projects register with minimal capital, rent luxury office spaces, yet pay no local taxes; their funds are kept outside the Singaporean banking system, while their spending contributes to rising housing prices, wage inflation, and the soaring cost of Certificates of Entitlement (COEs).

This has led to growing public dissatisfaction, and with local voters unimpressed, the government has little incentive to support an industry that yields political costs without proportional public benefit.

Industry Impact Assessment: Who Will Be Affected, and Is a Web3 Exodus Coming?

1.Affected Groups:

Individual Practitioners:

This includes independent developers, crypto advisors, market makers, miners, KOLs (crypto influencers), community managers, project founders, and business development personnel. In the past, individuals engaging in Web3 work in Singapore were generally not subject to licensing requirements. Under the new rules, however, every role may now be under regulatory scrutiny.

For example:

An independent developer writing smart contracts for an overseas blockchain project,

A consultant providing token issuance strategies,

A KOL publishing token analysis —All these activities could theoretically be classified as "providing digital token services."

Unlicensed Entities:

This includes crypto exchanges that have not yet obtained a PSA license (whether centralized CEXs or decentralized DEXs), DeFi project teams, NFT marketplaces, crypto wallet providers, cross-border payment networks, and a wide range of blockchain startups. If these entities have operations or legal registration in Singapore but hold no relevant licenses, they are among the most vulnerable, facing imminent business disruption risks.

This is especially true for early-stage startups that had established a Singapore base but targeted overseas markets—if they fail to meet the licensing criteria, they may effectively face "suspended execution" and be barred from continuing operations in Singapore. According to the new regulations, such entities must cease regulated activities by June 30 at the latest—otherwise, they will be considered operating illegally.

2.Exempted Entities:

Entities Already Licensed or Exempted Under PSA/SFA/FAA Are Not Required to Reapply for a DTSP License Under FSMA—But Must Fulfill Additional FSMA Obligations

Typical Example – Custodians:

If a custodian is already licensed or exempted under the Payment Services Act (PSA), it is not required to obtain a separate DTSP license under FSMA, even when serving overseas clients. However, it must comply with FSMA's additional regulatory obligations in areas such as technology, audit, and AML/CFT compliance.

FSMA Additional Compliance Requirements:

1. Technology Risk Management (TRM):

System architecture, backup procedures, penetration testing, and use of third-party service providers must align with industry best practices.

2. Annual Independent Audit Reports:

Must cover both financials and system controls, and be submitted within prescribed timelines.

3. Enhanced AML/CFT Requirements:

Stricter Know-Your-Customer (KYC), transaction monitoring, and suspicious transaction reporting obligations.

4. Mandatory Reporting of Major Security Incidents Within 1 Hour:

Incidents such as data breaches, private key compromise, or extended service outages must be immediately reported to MAS.

5. Ban on High-Value Cash Transactions:

All cash payments of S$20,000 or more are strictly prohibited.

The Formal Implementation of Singapore's DTSP Licensing Regime Marks the End of the Regulatory Arbitrage Era and the Start of a New PhaseAmid a global trend toward stricter crypto regulation, major jurisdictions are gradually addressing long-standing regulatory gaps around digital asset activities. Singapore stands out as one of the more aggressive examples in this shift.

The once-popular model of "setting up in Singapore and serving overseas clients" has now been uniformly brought under regulatory oversight—sending a clear message to the industry: the future of Web3 must be built on a foundation of legal and regulatory compliance. Singapore is also seeking to consolidate fragmented regulatory responsibilities previously spread across the PSA, SFA, and FAA, aiming to eliminate regulatory gray zones. The focus of oversight is shifting from merely "whether a license is held" to "whether operations are compliant."

Stablecoin regulation is also being upgraded in parallel:

● Single-Currency Stablecoins (SCS): Governed under a dedicated regulatory framework.

● Other Stablecoins: Continue to be treated as Digital Payment Tokens (DPTs) under the PSA;

however, if used as underlying assets in derivatives, they may fall under the SFA.

In short, the room for regulatory loopholes is rapidly shrinking.

Compliance-first operations are becoming the norm, and the era of exploiting jurisdictional differences to "game the system" is coming to a close.

If the period from 2018 to 2021 saw many Asian crypto entrepreneurs seeking regulatory "havens," then post-2025, those that remain standing will largely be firms that embrace regulation and possess real compliance capabilities.

Across the region, major financial centers are now competing to roll out clear regulatory frameworks.

Rather than a narrative of companies "fleeing" one jurisdiction, it is more accurate to say they are seeking the regulatory environments best aligned with their business models.

Two Self-Assessment Questions for Industry Participants

1. Am I currently licensed or exempted under the PSA/SFA framework?

2. Do I provide any digital token services to overseas clients?

If the answer to Question 1 is "Yes", a new license is not required, but compliance upgrades must begin immediately.

If the answer to Question 1 is "No", you must either obtain a license or shut down operations by June 30.

MAS's regulatory screws are only going to tighten further—don't wait until the last day to act. Licensed entities should treat compliance upgrades as an ongoing obligation.

Unlicensed teams without a full compliance strategy should urgently decide whether to apply, consolidate, or exit.

The lack of a transition period and MAS's demand for immediate cessation of unlicensed activities sends a clear message: Singapore will not serve as a safe haven for unregulated crypto businesses. Even though it was once viewed as a "crypto-friendly" jurisdiction, regulatory loopholes will no longer be tolerated.

MAS's actions confirm that Singapore's crypto regulatory environment has tightened significantly. Many local companies now face a hard choice: bear the high cost of licensing, or restructure their business or exit offshore markets. The government is willing to absorb short-term industry outflows if that's the price for preserving Singapore's international reputation and financial integrity.

Indirect Beneficiaries in the Region

Singapore's Move May Indirectly Benefit Other Jurisdictions, Reshaping Asia's Crypto LandscapeSingapore's tightening of crypto regulations may indirectly benefit other regions, prompting a new wave of geographic redistribution and regulatory specialization within Asia's digital asset ecosystem.

As another major crypto hub in the region, Hong Kong has in recent years aggressively promoted the legalization and regulatory development of virtual assets.

Just as Singapore clamps down, Hong Kong is actively positioning itself to absorb displaced crypto businesses. Hong Kong Legislative Council member and National Committee member of the Chinese People's Political Consultative Conference (CPPCC), Wu Jiezhuang, posted on social media noting that Singapore had earlier published its Guidelines on Licensing for Digital Token Service Providers, introducing new rules for companies, institutions, and individuals engaged in virtual asset activities.

Since Hong Kong's Virtual Asset Policy Statement in 2022, the city has welcomed the development of the Web3 industry. According to informal estimates, over 1,000 Web3 companies have established a presence in Hong Kong. Wu extended an open invitation to crypto firms currently operating in Singapore to relocate their headquarters and teams to Hong Kong, offering policy guidance and support for local setup. The underlying ambition: to position Hong Kong as Asia's leading crypto hub.

Link:

https://x.com/agintender/status/1930471612379471933?s=19

https://x.com/agintender/status/1930483789689696527?s=19

https://x.com/agintender/status/1930295802062352709?s=19

https://x.com/Johnny_nkc/status/1930220824629522613?t=Y_x1ZyMAUrcWeNIvKJ37SA&s=19

https://x.com/alexzuo4/status/1930566675721761129?t=LTpNuTZ9-b_w6FNXAqe13w&s=19

https://www.mas.gov.sg/-/media/guidelines-on-licensing-for-digital-token-service-providers.pdf

Follow us

Twitter: https://twitter.com/WuBlockchain

Telegram: https://t.me/wublockchainenglish

Great insights! Crypto regulation is definitely evolving rapidly, and staying updated is key.

Here’s our recent report with Bybit and Block Scholes that includes a deep dive into US crypto regulations: https://blockscholesresearch.substack.com/p/bybit-x-block-scholes-crypto-insights-report-deep-dive-into-us-crypto-regulations