The Uniswap protocol fee distribution proposal ignites the market, analysis of future trends

Author: defioasis

On the evening of February 23, Uniswap Foundation’s Gov Lead, Erin Koen, proposed to the Uniswap governance forum, suggesting the use of a fee mechanism to reward UNI token holders who have delegated and staked their tokens. Since Uniswap announced the token airdrop in late September 2020, there has been ongoing discussion about whether UNI should capture protocol fees to increase token utility, but almost all have fizzled out. This proposal by the head of the Uniswap Foundation formally brings the discussion of UNI token utility to the governance level, thereby causing a frenzy among holders and driving up the price of UNI and other DeFi protocol tokens.

Firstly, it’s important to clarify that this proposal was put forward by representatives of the Uniswap Foundation, which is not the same as Uniswap Labs. Uniswap Labs is responsible for the development, maintenance, and updates/upgrades of the Uniswap protocol, playing a central role in technical development and innovation. Essentially, Uniswap Labs is a commercial company. The Uniswap Foundation, on the other hand, primarily focuses on the governance and community development of the Uniswap protocol and is a non-profit organization. Uniswap Labs tends to consider issues from the protocol/company perspective, while the Uniswap Foundation represents community interests to a certain extent. It’s noticeable that the official Uniswap Labs social media has not mentioned or shared this matter, and even Uniswap protocol founder Hayden has not participated much in the discussion.

Secondly, it’s necessary to understand what protocol fees entail. Currently, there are two types of fees: front-end fees and LP (Liquidity Provider) fees. Front-end fees refer to the 0.15% fee charged since mid-October 2023 for transactions executed through the Uniswap Labs front-end, i.e., fees collected from the official Uniswap front-end and paid to Uniswap Labs; Hayden stated that the purpose of collecting this fee is to fund the sustainable operation of Uniswap Labs. LP fees are the fees charged by the Uniswap pools, paid by traders to LPs, such as the 0.3% fee collected by the WBTC/ETH pool with the highest TVL in Uniswap V3. The proposal specifies that protocol fees are expressed as a fraction of LP fees, which can be 0, 1/4, 1/5, 1/6, 1/7, 1/8, 1/9, or 1/10 (currently set to 0), and the specific fraction can be adjusted through governance.

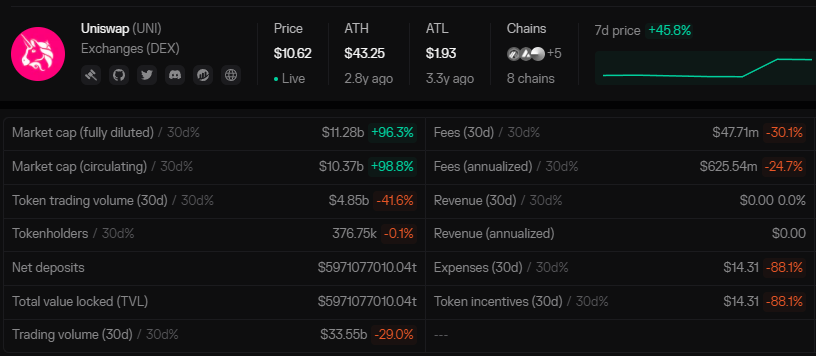

(Data Source: https://tokenterminal.com/terminal/projects/uniswap)

According to data from Token Terminal on February 25, the annualized LP fees for Uniswap are approximately $626 million. Assuming the proposal is passed and 1/10 to 1/4 of the LP fees are distributed as protocol fees to UNI holders, then UNI holders could receive approximately $62.62 million to $156.5 million in annual dividends. The current market cap of UNI is about $8 billion, with the market cap to annual dividend ratio ranging between 51.1 and 127.8. Of course, this is just a simple calculation for reference and not a basis for investment.

Finally, this proposal is still in the proposal and community discussion stage, and whether it will pass depends on the final vote by the community and UNI delegates representing various forces. The Uniswap Foundation believes that if there are no major obstacles, it is expected to post a Snapshot vote on March 1 and an on-chain vote on March 8. As an early investor in Uniswap, a16z could play a key role in the future vote on this proposal. According to Arkham data, addresses marked as a16z (and those suspected to be a16z) may control about 60 million UNI tokens.

Of course, nothing is set in stone yet, and the passage of the proposal remains uncertain, but it ultimately represents an attempt to transition to utility tokens. Even if this proposal ultimately fails, it is believed that other institutions or community leaders will continue to strive to convert UNI into a utility token. Additionally, if the proposal is passed, the impact of siphoning off a portion of LP earnings as dividends for token holders on LPs, and how to better balance the interests of UNI holders and LPs as the protocol evolves, will become new governance issues.

Over the years, Uniswap has arguably become the Beta that can represent the entire Crypto industry after BTC and ETH. Now that the foundation has formally proposed to empower UNI, this might be benefiting from favorable outcomes like the Grayscale and Ripple court victories, the smooth approval of spot BTC ETFs, increased trading activity, and relatively more lenient US regulatory policies. At the same time, this could also set an example for other protocol developers or teams, especially those in the United States. For instance, Blur and Blast founder Pacman has expressed approval of the proposal put forward by the Uniswap Foundation and hopes Blur can learn from it. (Note: The NFT trading market Blur’s token BLUR, similar to UNI, is also an unempowered governance token.)

Whether it’s UNI or BLUR, the protocols they represent are leaders in their respective fields. Uniswap occupies about 60% of the DEX market share, not only possessing outstanding technological innovation and market influence but also making an indelible contribution to the advancement of the Crypto industry, which are the core focuses of our continued attention. For Uniswap, empowering UNI might just be the icing on the cake, whereas the upcoming v4 hook might be even more exciting.

Follow us

Twitter: https://twitter.com/WuBlockchain

Telegram: https://t.me/wublockchainenglish