Tokenized U.S. Equities: Hype or Structural Breakthrough? Tracing Their Origins, Market Landscape, and Future Trajectory

Author | @Web3_Mario

Compiler | Wublockchain Aki

Original link:https://mp.weixin.qq.com/s/2aBb0wxcE-Gisvi5vdgztw

Summary:

As Trump’s policy agenda begins to take shape—using tariffs to bring manufacturing back onshore, deliberately triggering a stock market bubble to pressure the Federal Reserve into rate cuts and monetary easing, and accelerating industrial development through deregulation-driven financial innovation—this strategic combination is visibly reshaping the market landscape. Among these measures, the deregulation tailwind is drawing growing attention from the crypto industry to the RWA (Real-World Assets) sector. This article focuses on the opportunities and challenges of tokenized equities.

The Evolution of Tokenized Equities

In fact, tokenized equities are not a new concept. As early as 2017, attempts at STOs (Security Token Offerings) had already begun. STOs are a fundraising mechanism in the crypto space that essentially digitize and tokenize traditional financial securities by putting them on the blockchain. This process combines the regulatory compliance of traditional securities with the efficiency and programmability of blockchain technology. Among various security types, tokenized equities have emerged as one of the most prominent and closely watched applications within the STO ecosystem.

Before the advent of STOs, the predominant fundraising method in the blockchain space was ICOs (Initial Coin Offerings). The rapid rise of ICOs was largely driven by the convenience of Ethereum smart contracts. However, most ICO-issued tokens did not represent claims to real-world assets and were often unregulated, which led to widespread fraud and exit scams.

In 2017, the U.S. Securities and Exchange Commission (SEC) issued a statement regarding the DAO incident, declaring that certain tokens could be classified as securities and should therefore be subject to regulation under the Securities Act of 1933. This marked the official beginning of the STO (Security Token Offering) concept. By 2018, STOs gained traction as a “compliant alternative to ICOs” and started attracting attention within the industry. However, due to the lack of unified standards, poor secondary market liquidity, and high compliance costs, the overall market developed slowly.

With the arrival of the “DeFi Summer” in 2020, some projects began experimenting with decentralized solutions by using smart contracts to create derivatives pegged to stock prices. These approaches allowed on-chain investors to gain exposure to traditional stock markets without undergoing complex KYC procedures. This model, commonly referred to as synthetic assets, does not involve holding actual U.S. equities, and transactions do not rely on centralized intermediaries. As a result, participants could avoid costly legal and regulatory hurdles. Representative projects include Synthetix and Mirror Protocol from the Terra ecosystem.

In these models, market makers would mint synthetic U.S. equities by locking up excess crypto collateral and then provide liquidity for these assets. Traders could access them directly through DEXs on secondary markets to gain price exposure to the underlying stocks. At that time, Tesla was the star of the U.S. stock market—unlike Nvidia, which has dominated in the current cycle—so many projects promoted their platforms with slogans like “Trade TSLA directly on-chain.”

However, actual market development has shown that on-chain trading of synthetic U.S. equities has remained underwhelming. Take sTSLA on Synthetix as an example—even when including both primary market minting and redemption, the total number of on-chain transactions has only reached 798.

Subsequently, many projects publicly cited regulatory concerns as the reason for delisting synthetic U.S. equities and pivoted to other business verticals. However, the more fundamental issue was likely the failure to achieve Product-Market Fit (PMF) and the inability to establish a sustainable business model. The viability of the synthetic asset model depends on sufficient on-chain trading demand, which would attract market makers to mint synthetic assets in the primary market and profit from providing liquidity in the secondary market.

Without this level of demand, market makers not only fail to earn fees through synthetic trading but are also forced to bear the short exposure risk to the underlying U.S. equities they track. This disincentive further erodes liquidity and undermines the entire mechanism.

Beyond the synthetic asset model, some well-known centralized exchanges (CEXs) have explored offering U.S. stock trading access to crypto users through a custodial approach. In this model, real stocks are held by third-party financial institutions or the exchange itself, while corresponding tradable tokens are issued directly on the CEX platform.

Two notable examples are FTX and Binance. On October 29, 2020, FTX launched its tokenized stock trading service in partnership with German financial firm CM-Equity AG and Swiss-based Digital Assets AG. This allowed users—excluding those in the U.S. and other restricted jurisdictions—to trade tokens pegged to U.S.-listed equities such as Facebook, Netflix, Tesla, and Amazon.In April 2021, Binance also began offering tokenized stock trading services, with Tesla (TSLA) being the first equity listed.

At the time, however, the regulatory environment was far from favorable. Moreover, since the core initiators of these tokenized stock services were centralized exchanges (CEXs), they inevitably found themselves in direct competition with traditional stock trading platforms such as Nasdaq—drawing considerable scrutiny and pressure.FTX reached a peak in tokenized stock trading volume in Q4 2021, with October alone recording $94 million in trades. However, the service was discontinued following FTX’s bankruptcy in November 2022. Binance, on the other hand, halted its tokenized stock trading service just three months after launch, citing regulatory concerns. The suspension was officially announced in July 2021.

Subsequently, as the market entered a bear phase, development in this sector came to a standstill. It wasn't until Donald Trump’s election victory—and the pro-deregulation financial policies that followed—that regulatory conditions began to shift, reigniting market interest in tokenized equities. However, by this time, the concept had taken on a new name: RWA (Real-World Assets).This new paradigm emphasizes a compliance-first design, involving qualified issuers who tokenize real-world assets on-chain with a strict 1:1 backing. The entire lifecycle of the token—including issuance, trading, redemption, and collateral management—is conducted in full adherence to regulatory standards.

Current Market Landscape of Tokenized Equities

Let’s now examine the current state of the stock-based RWA market. Overall, this sector remains in its early stages and is still predominantly focused on U.S. equities. According to data from RWA.xyz, the total issuance volume of stock RWAs has reached $445.40 million. However, it is important to note that $429.84 million of this volume comes from a single asset: EXOD, a tokenized stock issued by Exodus Movement, Inc.

Exodus is a software company focused on developing self-custodial cryptocurrency wallets. Founded in 2015 and headquartered in Nebraska, USA, Exodus is listed on the NYSE American exchange. The company allows its Class A common shares to be migrated to the Algorand blockchain, where users can view the price of their on-chain holdings directly within the Exodus Wallet. The company currently has a total market capitalization of $1.5 billion.

Exodus has become the only U.S.-based company to tokenize its common stock on a public blockchain. However, it is important to note that the on-chain representation of EXOD is merely a digital marker of the company’s shares. It does not confer any voting, governance, economic, or other shareholder rights. Moreover, the token itself cannot be freely traded or transferred on-chain.

This event carries symbolic significance, marking a clear shift in the SEC’s stance toward on-chain equity assets. In reality, Exodus's attempt to tokenize its common stock was far from smooth.

In May 2024, Exodus initially filed an application to tokenize its Class A common shares. However, at that time, the SEC had not yet adjusted its regulatory position, resulting in the proposal being initially rejected. It wasn’t until December 2024—after continuous improvements to its technical framework, compliance mechanisms, and disclosure procedures—that Exodus finally secured SEC approval and successfully launched its tokenized equity on-chain.

The milestone also sparked strong interest in the company’s stock, which subsequently reached an all-time high in market price.

Apart from Exodus, approximately $16 million in market share is attributed to a project called Backed Finance, a Swiss-based company operating under a compliant framework. Backed allows KYC-verified users to mint tokenized equity assets on-chain via its official primary market by paying in USDC. Once it receives the crypto assets, Backed converts them into USD and purchases the corresponding stock (e.g., COIN) on the secondary market—though this process may experience delays due to traditional market hours.

Once the shares are successfully acquired, they are held in custody by a Swiss custodian bank. Backed then mints bSTOCK tokens on a 1:1 basis and delivers them to users. The redemption process follows the reverse flow.

To ensure reserve asset transparency and security, Backed works with an audit firm called The Network Firm, which regularly publishes proof-of-reserve reports. On-chain investors can also purchase these tokenized stocks directly via DEXs such as Balancer.Importantly, holders of these stock tokens do not gain any ownership rights to the underlying equities or any associated entitlements, such as voting rights. Only KYC-approved users are permitted to redeem USDC through the primary market.

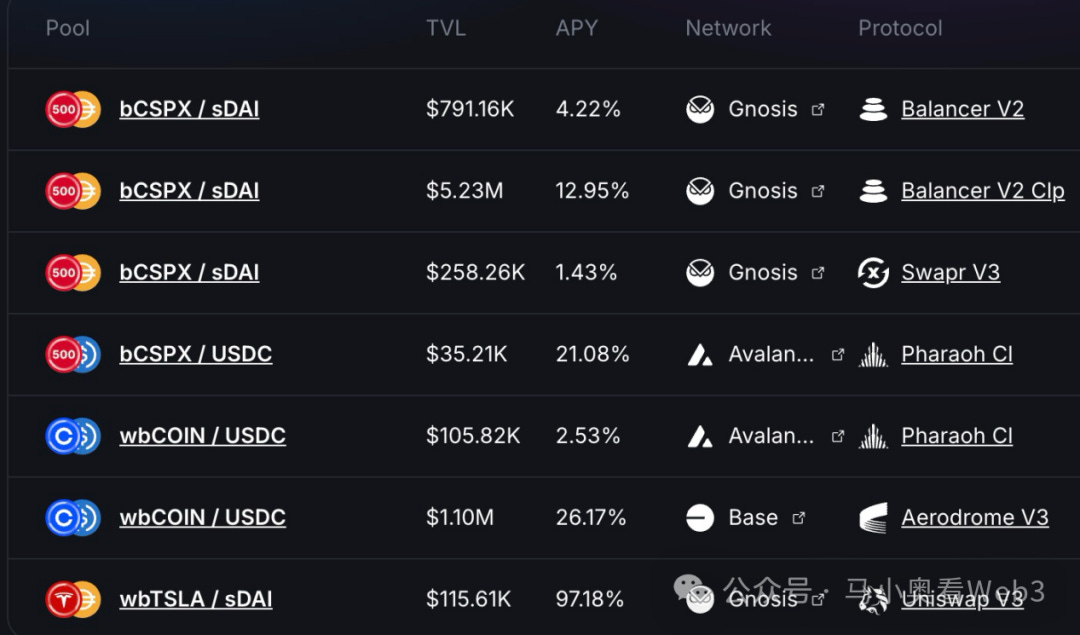

In terms of issuance volume, adoption of Backed’s tokenized assets is primarily concentrated in two products: CSPX and COIN. The former has an issuance volume of approximately $10 million, while the latter stands at around $3 million.

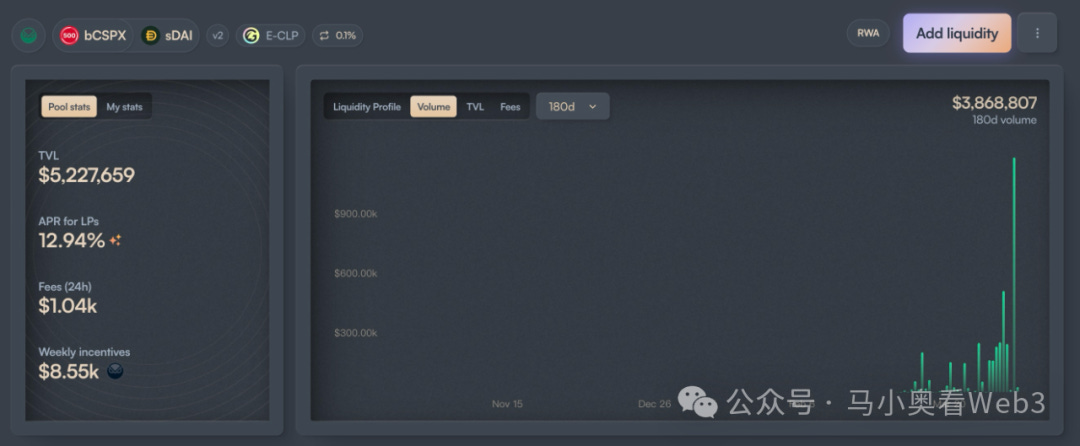

Regarding on-chain liquidity, activity is mainly distributed across the Gnosis and Base blockchains. bCSPX has about $6 million in liquidity, while wbCOIN holds around $1 million. However, trading activity remains relatively modest. For instance, the largest liquidity pool for bCSPX, deployed on February 21, 2025, has recorded a cumulative trading volume of approximately $3.8 million, with around 400 transactions in total.

Another notable development is the progress made by Ondo Finance. On February 6, 2025, Ondo announced its broader strategic initiative encompassing both the Ondo Chain and Ondo Global Markets. Within this framework, tokenized equities are positioned as a core asset class under Ondo Global Markets.

With its stronger TradFi (traditional finance) connections and more advanced technical infrastructure, Ondo may have the potential to accelerate the growth of this sector. However, its long-term impact remains to be seen.

Opportunities and Challenges of Stock-Based RWAs

Next, let’s explore the opportunities and challenges associated with stock-based RWAs. Generally speaking, the market recognizes three main advantages of tokenized equities:

● 24/7 Trading Platforms:Due to the technical nature of blockchain, tokenized equities can be traded on a 24/7 basis. This capability frees tokenized stock trading from the time constraints of traditional exchanges, unlocking previously untapped market demand.Take Nasdaq as an example. Although it has extended its services to include pre-market and after-hours trading to approximate 24-hour access, regular trading hours are still limited to weekdays. In contrast, building a trading platform directly on blockchain infrastructure allows for truly continuous trading at lower operational costs.

● Low-Cost Access to U.S. Assets for Non-U.S. Investors:Moreover, with the growing adoption of payment-based stablecoins, non-U.S. users can directly use stablecoins to trade U.S. assets—avoiding the costs and delays associated with cross-border and interbank transfers.For example, if a Chinese investor uses Tiger Brokers to invest in U.S. equities, the cross-border remittance fee alone (excluding currency conversion fees) is approximately 0.1%. Additionally, settlement typically takes 1 to 3 business days. In contrast, on-chain transactions can eliminate both the remittance cost and the settlement delay.

● Composability Unlocks Financial Innovation:Thanks to their programmability, tokenized equities are well-positioned to integrate with the broader DeFi ecosystem, unlocking far greater potential for on-chain financial innovation. This enables use cases such as on-chain lending, among others.

However, in the author’s view, tokenized equities currently face two key areas of uncertainty:

● Pace of Regulatory Progress:Based on the cases of EXOD and Backed, it is evident that current regulatory frameworks still fall short in resolving the issue of "token-share equivalence"—that is, ensuring that holders of tokenized equities enjoy the same legal rights as holders of traditional shares, including governance rights.This legal gap limits many potential use cases, such as utilizing secondary market holdings in corporate mergers and acquisitions. Moreover, the lack of clear, compliant use cases for tokenized stocks continues to hinder financial innovation. As a result, the sector’s progress remains highly dependent on the pace of regulatory reform.Given that the current Trump administration is still prioritizing reshoring manufacturing as a core policy objective, any significant movement on tokenized equity regulation may be further delayed.

● The Evolution of Stablecoin Adoption:From a historical perspective, the core target users of tokenized equities are likely not crypto-native participants, but rather traditional, non-U.S. investors interested in the U.S. stock market. For this demographic, the rate of stablecoin adoption remains a key issue worth monitoring, as it is closely tied to each country’s regulatory stance on stablecoins.For example, Chinese investors face a 0.3% to 1% premium when acquiring stablecoins through OTC markets, compared to using official currency exchange channels. This premium is significantly higher than the cost of investing in U.S. stocks through traditional financial institutions.

In summary, the author believes that stock-based RWAs present two key market opportunities in the short term:

1. For publicly listed companies:By referencing the case of EXOD, listed firms can issue on-chain representations of their shares. Although real-world use cases remain limited in the short term, the potential for financial innovation alone may lead investors to assign higher valuations to such companies.For example, enterprises that offer on-chain asset management services could leverage tokenized equities to convert their investors into product users. At the same time, the shares held by these investors could be counted as assets under management (AUM), thereby enhancing the company’s perceived growth potential.

2. For tokenized high-dividend U.S. equities:Tokenized high-dividend U.S. equities may attract adoption from yield-generating DeFi protocols. As market sentiment shifts and most native on-chain real yield opportunities experience a significant decline in returns, protocols like Ethena—which aim to maintain competitive yields—must continuously seek new sources of sustainable, real-world yield. A relevant example is Ethena’s allocation to BUIDL.High-dividend stocks, typically found in mature industries with stable business models and strong cash flows, are able to consistently distribute profits to shareholders. These equities often exhibit low volatility and strong resistance to economic cycles, making them relatively low-risk investments. If tokenized blue-chip dividend stocks become available, they could offer a compelling option for DeFi protocols seeking more reliable, yield-generating assets.

Follow us

Twitter: https://twitter.com/WuBlockchain

Telegram: https://t.me/wublockchainenglish