Understanding the 'Yield-Focused' L2 Blast Launched by Blur's Founder: Sources of Returns and Raised Concerns

Author: defioasis

On November 21, coinciding with the announcement of the end of Blur S2 and the start of S3, Blur’s founder Pacman launched Blast, an OP Rollup-based layer2 with inherent ETH and stablecoin yields, along with the BLUR staking system. Blast secured $20 million in funding from investors including Paradigm and Standard Crypto. Utilizing an invitation mechanism and a point system that rewards transparent airdrops, by November 26, in less than six days, Blast had accumulated over $520 million in funds. This includes more than 220,000 ETH staked in Lido and over 64 million DAI in Maker DSR. Compared to other L2 solutions, Blast has surpassed zkSync Era, becoming the fourth largest L2.

However, strictly speaking, Blast cannot yet be classified as L2, but rather as an intermediary contract that deposits and locks assets, allowing deposits but no withdrawals before its mainnet launch. Its basic principle is to accept users’ ETH or stablecoins, staking the ETH in Lido and converting stablecoins into DAI for staking in Maker.

Concerns and Responses The market’s main concerns about Blast revolve around two aspects: contract security and its “brutal” model.

Addressing security concerns, L2Beat pointed out that although the Blast contract (0x5f…a47d) is referred to as LaunchBridge, it is not actually a Rollup Bridge but a simple custodial contract protected by a 3/5 multisig address. Blast lacks the validity proofs required for an L2 state root or a fraud-proof mechanism. Polygon Developer Relations Engineer Jarrod Watts further noted that the five signatories of the Blast multisig contract are new, unidentified addresses; Blast is not an L2, lacking a testnet, transactions, a bridge, rollback capabilities, and transaction data transmission to Ethereum. He also mentioned the contract’s authorization of any “mainnetBridge” to spend the maximum possible amount of its Lido and DAI holdings. Cos, the founder of SlowMist, highlighted potential risks, including the upgradability of the Blast contract, its owner 3/5 multisig without a time lock; to abscond with funds, the multisig could either upgrade to a malicious logic contract or set a malicious mainnetBridge through enableTransition. In response to these security concerns, Blast officials replied that time locks could reduce the security of smart contracts, and in complex contracts, the security of upgradable contracts might surpass that of immutable ones. They emphasized that each key in the multisig is independently secure, should be stored in cold storage, managed by independent parties, and geographically separated. They plan to update one of the multisig addresses within a week to switch the underlying hardware wallet provider, ensuring that no single type of hardware wallet is used in 3 out of 5 instances. This approach maintains security even in unprecedented hardware wallet damage scenarios.

Regarding Blast’s “brutal” approach, it can be broadly categorized into two aspects: technical and operational.

Technical Simplicity: It’s a so-called L2 with hardly any features, relying solely on a simple intermediary custodial contract to attract hundreds of millions of dollars in locked-up assets. This approach has quickly surpassed the advantages accumulated by other well-known public chains over half a year or even more than a year.

Operational brutality: Reusing the criticized invitation mechanism and point system from Paradigm’s major projects, Blur and friend tech, and combining this with mandatory lock-up before the mainnet launch and a leaderboard closely related to airdrops, exploits users’ tendency to chase airdrops and their psychological inertia when it comes to unrewarded long-term engagement, leading to a FOMO among players.

Although the Blast model is indeed “ugly”, it is actually rational. It is backed by renowned institutions and follows the precedents set by successful projects. There are real revenue sources and calculable APY, along with a clear expiration date. Depositing ETH/stablecoins in Blast essentially equates to DeFi lock-up mining. The base yield is provided by Lido or Maker, and the future Blast airdrops that can be exchanged for points represent the mining profits.

The Impact on Other L2 Chains

While some viewpoints suggest that the emergence of Blast could create a shockwave for other L2 chains, or even pressure them to offer more explicit airdrop incentives, the reality is that Blast’s rapid achievement of over $500 million in TVL is not a result of draining resources from other L2.

Since November 21 at 00:00 UTC, the TVL of the top four L2 chains has all shown growth. The largest decline in TVL for Linea appears to have little connection with Blast. Linea’s TVL dramatically increased from $86.5 million on November 15 to a peak of $263 million on November 23, primarily due to the liquidity integration with cross-chain bridges Orbiter and Rhino. Data from Arkham indicates that addresses suspected to be associated with Orbiter (0x3F…6372 & 0xA7…73cE) and Rhino (0xC4…5eCB) contributed a net inflow of nearly 50,000 ETH to Linea in the week prior to November 23. The subsequent decline in TVL is also linked to the withdrawal of liquidity from Orbiter and Rhino, possibly as part of a liquidity test for Linea’s cross-chain operations.

After removing the outliers, the chart becomes clearer. This includes the TVL of mature top-tier L2s with issued tokens like Arbitrum and Optimism, as well as highly anticipated ones like Base, zkSync Era, Mantle, and StarkNet, all showing positive growth. The impact of Blast’s emergence on other L2 Chains may be much smaller than what the market noise suggests.

Given that the core data of mainstream L2s is not significantly affected, it’s less likely that they would be compelled to release more precise airdrops or offer more substantial incentives. Most are expected to maintain their current status and operational strategies. In fact, compared to other L2 activities like Odyssey, where the relationship with airdrops is unclear, Blast’s transparent airdrop strategy based on a point system represents merely a change in the airdrop acquisition strategy rather than a direct competition in underlying technology and ecosystem applications. Therefore, it can be observed that the foundations of most other major L2 chains remain stable and are not significantly affected by the emergence of a new entity.

The funds absorbed by Blast are likely mainly from idle funds. The primary reason for idleness is the reduced yield in DeFi, especially as there are few stable mining pools suitable for large capitals. Blast, offering “basic yield rates from Lido/Maker + mining profits from airdrops exchangeable for points,” backed by institutions and with substantial returns, is highly attractive to those seeking stable returns and manageable risk.

The Impact on Blur

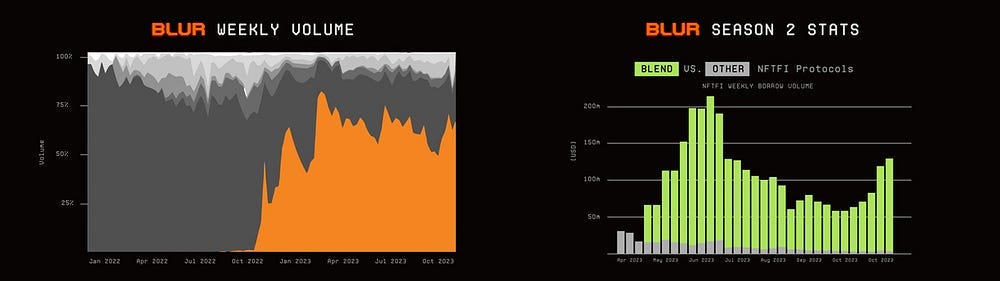

With the launch of Blast, Pacman also introduced a staking mechanism for BLUR, allowing users to earn points representing airdrops. The S3 airdrop is set to be equally split between NFT traders and BLUR stakers. As of November 26, 336 million BLUR tokens have been staked, valued at over $200 million, exceeding 10% of the total supply.

While there is no explicit connection between Blast and Blur, Blast should be viewed as a part of Pacman’s strategy to expand the NFT trading market footprint of Blur, similar to the lending platform Blend. According to official data, during S2, Blur achieved a trading volume of $6.1 billion with over 260,000 users, averaging a 65% market share. This success has firmly positioned Blur ahead of OpenSea, making it the leading platform in the Ethereum NFT trading market. Alongside its solid footing in the spot market, Blur’s lending market, Blend, has rapidly captured a major share in the NFT lending sector, demonstrating a strong Matthew effect where the ‘strong get stronger’. Both Blur and Blend have secured significant market shares in their respective domains and are self-sustaining with stable income streams. They form the foundation for continued expansion, countering the pessimistic view held by some that Pacman might abandon Blur to start anew with Blast.

(Source: https://x.com/blur_io/status/1726755862423990409?s=20)

Considering the reference to CEX token trading, where futures trading volume is often several times that of spot trading and is one of the core sources of revenue, experimenting with NFT perps seems promising. Unlike the firm hold of CEXs on FT futures trading, the resistance to chain-based NFT Perp is significantly lower, although the high gas fees on Ethereum present a challenge.

Pacman sees the two biggest opportunities in NFTs as lowering transaction costs and developing institutional-level NFT Perps (perpetual contracts). This underlines the need for L2 solutions. The Blur Bid Pool, holding tens of thousands of ETH but unable to enjoy earnings, poses an issue that could be addressed with the launch of an L2. Hence, Blast, with its underlying staking returns, emerged at an opportune time. In the future, the ETH in Blur’s Bid Pool is likely to be deposited in Blast, in return for blurETH for trading. This allows trading while still enjoying native ETH staking returns. It’s even possible that in the future, instead of relying on Lido, it could establish its own native staking protocol. Moreover, significantly reduced transaction costs may in turn stimulate more spot trading volume.

If blurETH from the Bid Pool built on Blast could directly serve as a trade pair asset for NFT Perps or include some composability similar to GLP, this could unleash greater liquidity.

As an L2, Blast will inevitably open up to more protocols and developers, and it’s not impossible for Paradigm to create a super dApp on Blast akin to friend tech. To capture users and give back to the community, these new applications might consider airdropping to Blast users and those closely associated with Blur.

Follow us

Twitter: https://twitter.com/WuBlockchain

Telegram: https://t.me/wublockchainenglish